Crocs Inc. (CROX): Buying a $1 Billion Footwear Franchise at 5× EBIT

"You will be right, over the course of many transactions, if your hypotheses are correct, your facts are correct, and your reasoning is correct." - Warren Buffett

Executive Summary

The idea initially surfaced while reviewing recent 13F filings from Himalaya Capital, the investment firm led by Li Lu. His purchase prompted a deeper look at the underlying economics of the Crocs Brand and the unusually low valuation currently assigned to the business. Crocs represents one of the most unusual valuation gaps currently available in public markets.

At roughly $83 per share, Crocs trades at:

~8× free cash flow

~4.8× Crocs Brand EBIT

Yet the Crocs Brand alone generates:

These margins rival the best consumer footwear brands in the world.

The market, however, is valuing the company as if the entire business were impaired following the failed HEYDUDE acquisition.

In reality, the Crocs Brand remains one of the most profitable footwear businesses globally.

The investment thesis is straightforward:

Crocs does not require growth or multiple expansion to generate attractive returns.

At current prices:

the free cash flow yield is roughly 16%

buybacks reduce share count 8–10% annually

Even if the market never re-rates the business, these economics alone can compound per-share value meaningfully.

The Crocs Story: From Ridicule to Global Brand

Crocs was founded in 2002 around a distinctive product: a foam clog made from proprietary Croslite material.

The design was widely mocked but had several advantages:

extremely lightweight

waterproof

antimicrobial

easy to clean

durable

The product quickly gained adoption in professions prioritizing comfort over aesthetics:

healthcare workers

restaurant staff

hospitality workers

parents purchasing children’s footwear

From the beginning, Crocs was not purely a fashion product. It was a functional footwear solution.

The First Cycle: Growth and Collapse

Crocs exploded in popularity during the mid-2000s.

By 2007:

Revenue exceeded $800M

The stock traded above $70

The financial crisis exposed weaknesses in the company’s strategy.

Aggressive retail expansion and inventory mismanagement damaged the brand.

Between 2008 and 2016, Crocs experienced nearly a decade of stagnation:

revenue stabilized near $1–1.2B

operating margins disappeared

the brand became deeply unfashionable

Many investors concluded Crocs had been a temporary fad.

Yet even during this trough, Crocs continued selling over $1B annually.

That observation matters today: the brand possesses a functional demand floor independent of fashion cycles.

The Turnaround Under Andrew Rees

Crocs’ revival began when Andrew Rees became CEO in 2017.

Rees implemented four strategic changes.

1. Retail Rationalization

Crocs closed hundreds of stores and shifted toward:

wholesale distribution

direct-to-consumer e-commerce

2. Product Focus

The company returned to its signature product:

the classic clog

3. Brand Repositioning

Rather than chasing traditional fashion credibility, Crocs embraced its unconventional identity.

Celebrity collaborations included:

Post Malone

Justin Bieber

Bad Bunny

Balenciaga

These collaborations repositioned Crocs as a self-aware anti-fashion brand.

4. Digital Expansion

Direct-to-consumer channels expanded rapidly.

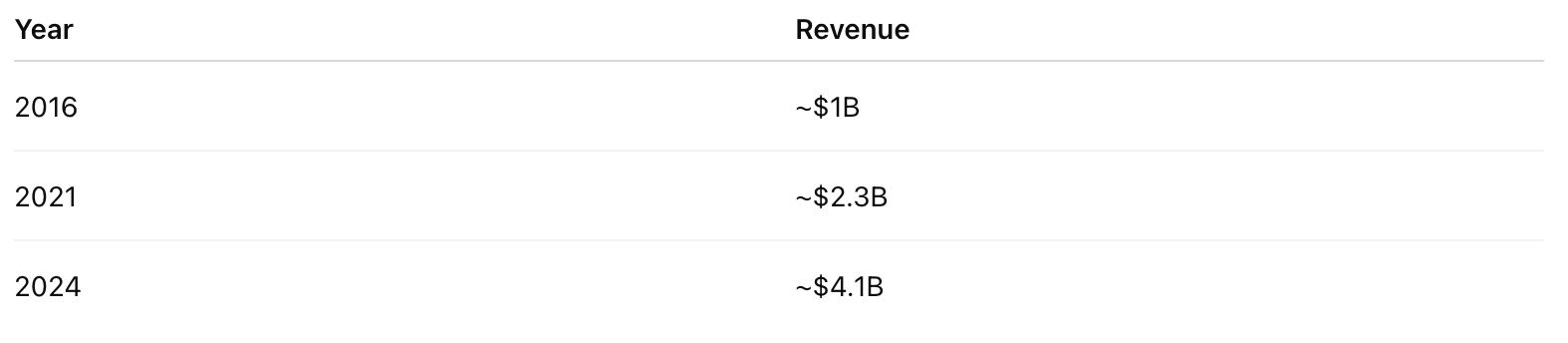

The Result

The turnaround produced dramatic growth.

Importantly, this growth required minimal capital investment because Crocs outsources manufacturing.

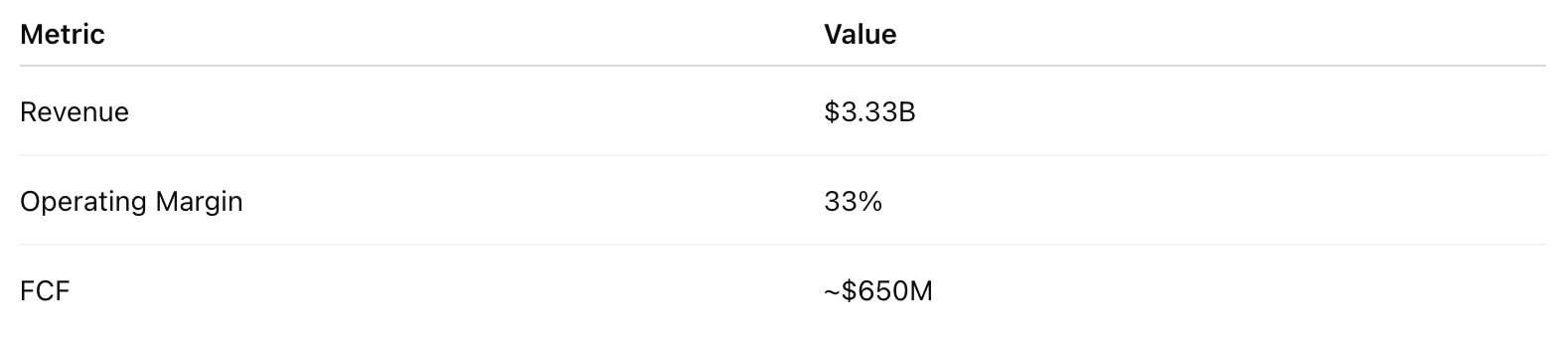

Crocs Today: Exceptional Economics

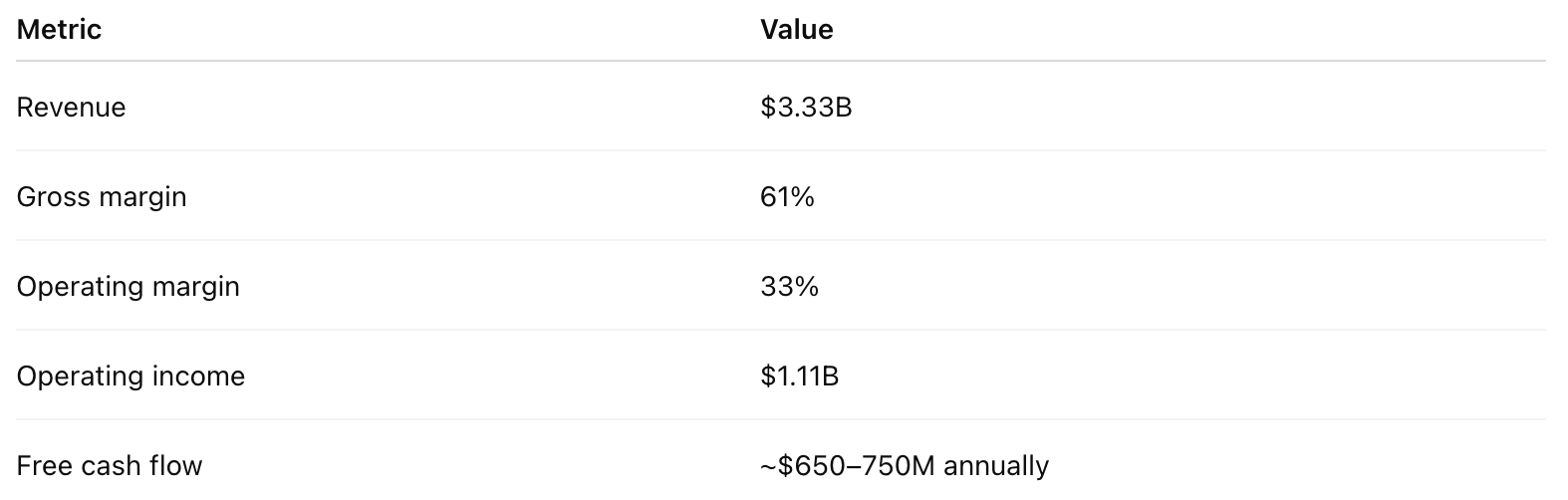

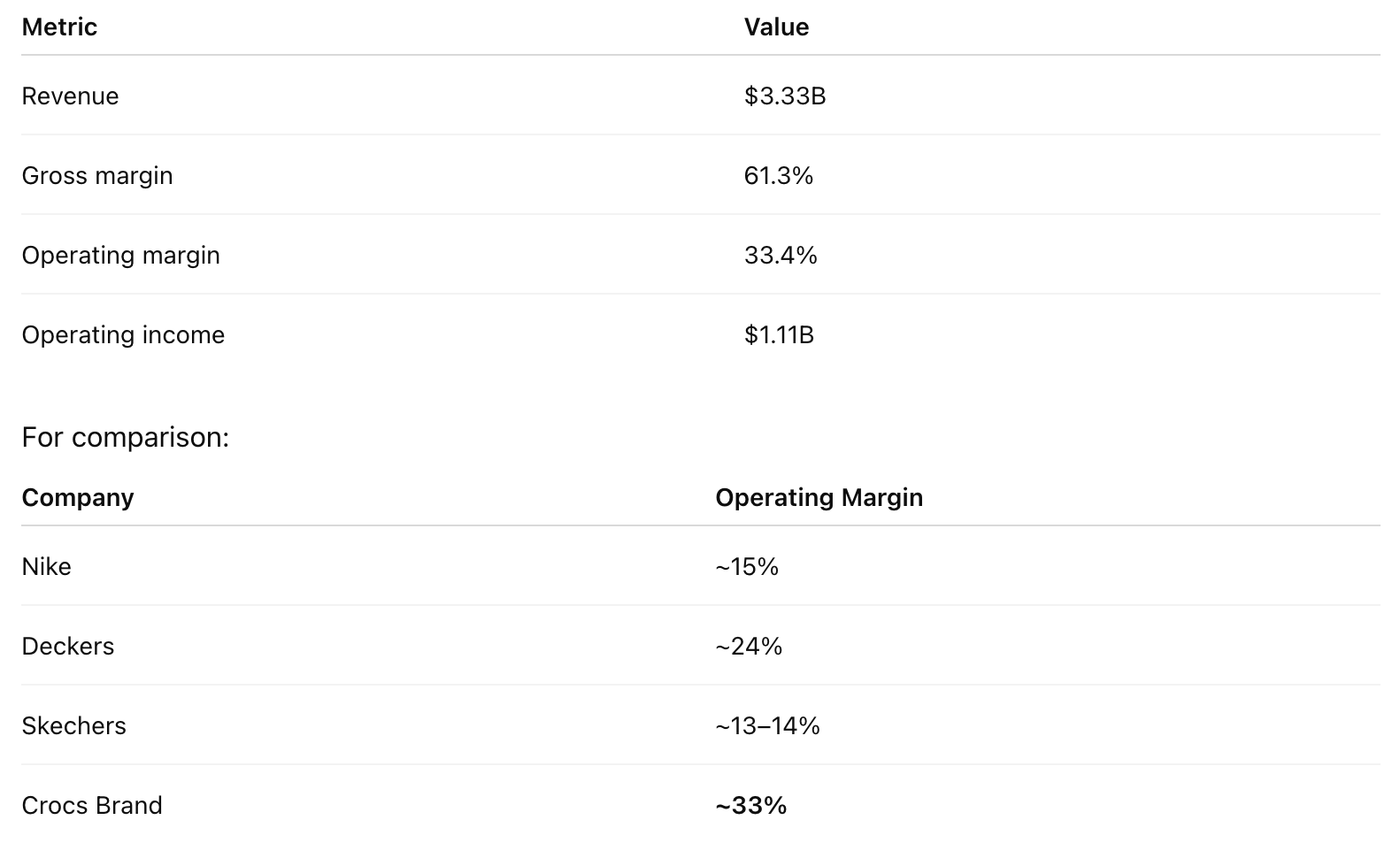

The Crocs Brand alone produces remarkable profitability.

FY2025 Crocs Brand (Excl. HEYDUDE)

This level of profitability is extremely unusual for footwear.

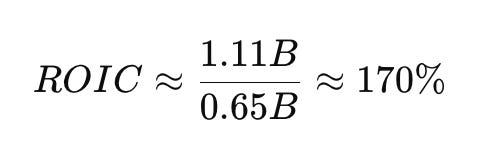

Capital Efficiency

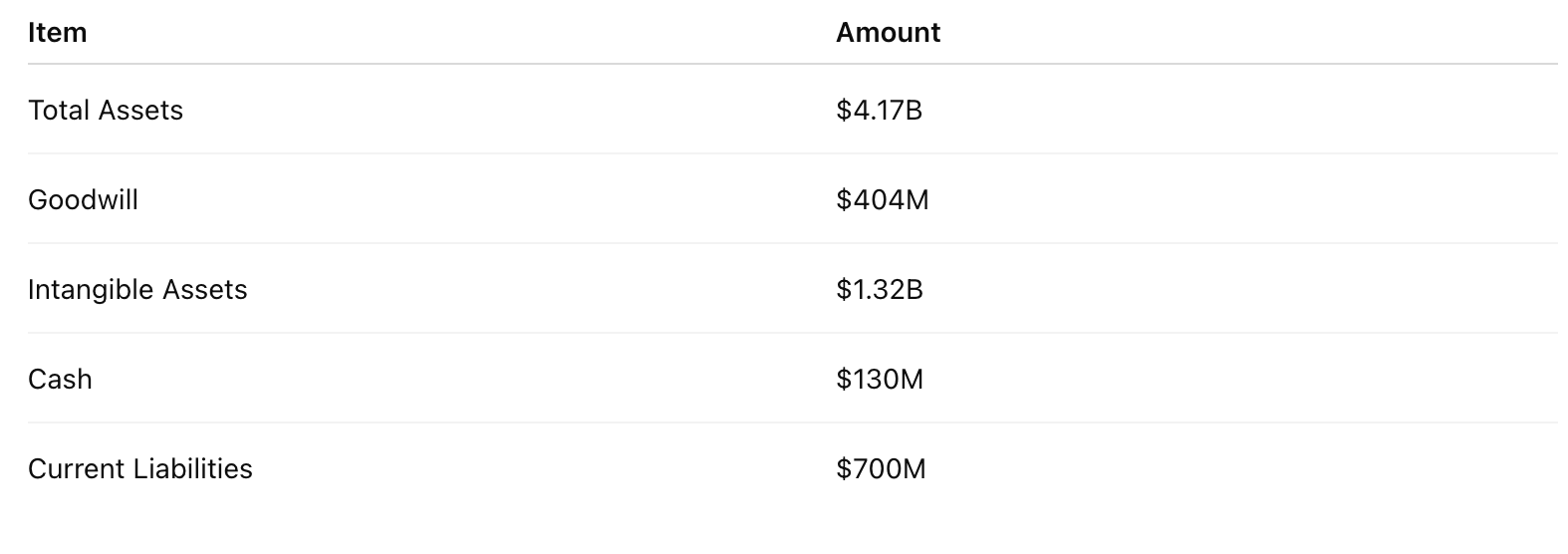

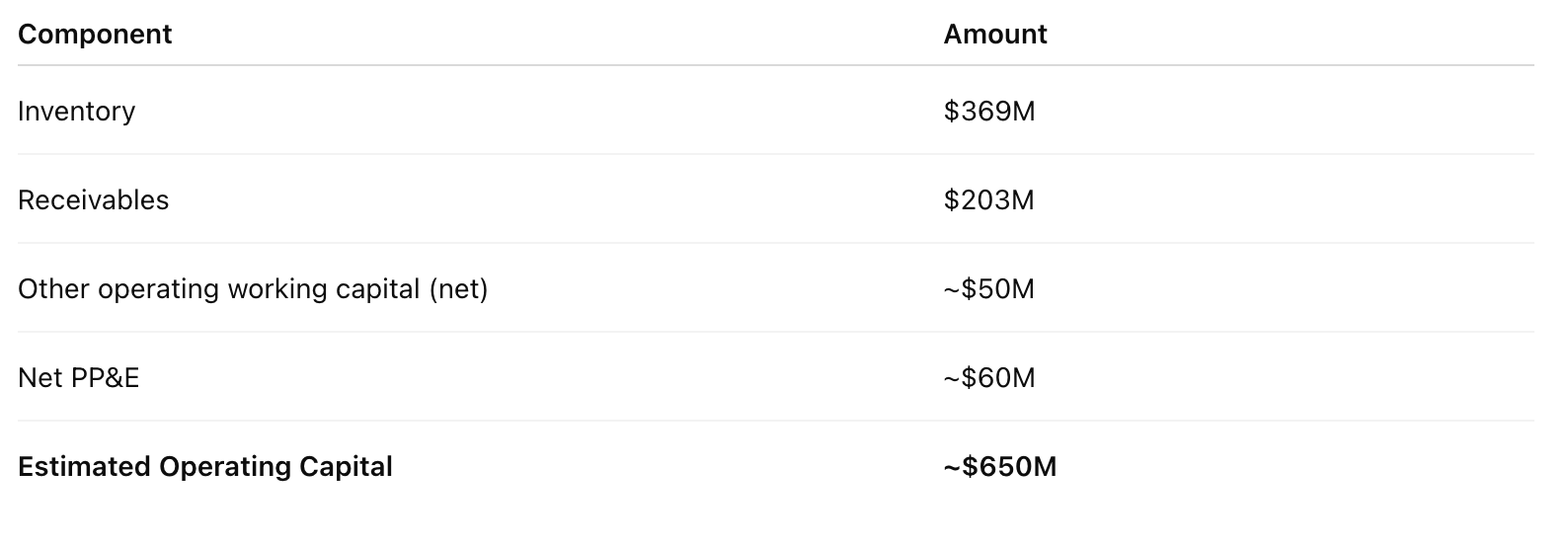

One of the most striking features of the Crocs business model is its extremely high return on capital. However, the headline figure requires a clear derivation to be meaningful.

Crocs reports total assets of approximately $4.17B as of FY2025. Much of this capital base relates to the HEYDUDE acquisition and does not represent capital required to operate the Crocs Brand.

To estimate the economic capital employed by the Crocs Brand, we adjust the balance sheet as follows:

Reported Balance Sheet (FY2025)

The majority of goodwill and intangible assets relate to the HEYDUDE acquisition and represent purchase accounting rather than operating capital.

For an economic capital estimate, we focus on the capital required to support Crocs Brand operations:

Economic Capital Bridge

This produces an estimated operating capital base of roughly $600–650M.

Against Crocs Brand operating income of approximately $1.11B, this implies:

Return on Operating Capital:

Even allowing for estimation error, the returns remain exceptional.

The key reason is structural: Crocs designs and markets footwear but does not own manufacturing assets, allowing the business to scale without meaningful capital investment.

Few consumer brands operate with this level of capital efficiency.

The HEYDUDE Acquisition

In 2022 Crocs acquired HEYDUDE (HD) for roughly $2.5B.

The goal was diversification beyond the clog category.

The acquisition proved problematic.

HD experienced:

declining revenue

inventory mismanagement

brand fatigue

In 2025 Crocs recorded approximately $738M of impairment charges related to HD.

These impairments created several distortions:

negative EPS

abnormal tax rates

confusing segment reporting

Many investors stopped analyzing the company at this point.

The Core Mispricing

Crocs Brand operating income:

~$1.11B

Current enterprise value:

~$5.3B

Which implies:

EV / Crocs Brand EBIT ≈ 4.8×

HD is effectively being valued at zero or rather, negative value.

A Historical Parallel: American Express (1963)

This mispricing structure resembles Warren Buffett’s investment in American Express during the salad oil scandal.

The scandal created large accounting losses that caused the market to treat the entire company as broken.

Buffett recognized that the core franchise remained intact.

He bought the company while the market priced the whole business as damaged.

Crocs today exhibits a similar structure:

HD is the scandal

the Crocs Brand is the intact franchise

One key difference exists: the salad oil scandal was a discrete event with a known liability, while HD remains an ongoing operational issue.

Nevertheless, the structural logic is similar.

Demand Durability

Crocs sold roughly 129M pairs in FY2025.

Despite:

tariffs

cautious wholesale partners

declining North American revenue

fashion skepticism

unit volumes still increased slightly.

Demand comes from two segments.

1. Utility Buyers

Healthcare workers, hospitality staff, and parents buying children’s shoes.

2. Casual Buyers

Consumers purchasing Crocs for everyday comfort.

This combination creates a demand base more durable than typical fashion brands.

Replacement vs Collection Behavior

Crocs behaves less like a replacement product and more like a collection product.

Consumers often own multiple pairs:

work pair

house pair

outdoor pair

seasonal colors

The Jibbitz charm ecosystem reinforces this behavior by turning the clog into a customizable platform.

The Jibbitz Ecosystem

One underappreciated element of the Crocs business model is the Jibbitz charm ecosystem.

Jibbitz are small decorative accessories inserted into the holes of Crocs clogs. While individually inexpensive, they carry extremely high margins and reinforce customer attachment to the brand.

The economic significance of Jibbitz is not just the accessory revenue itself but the behavioral pattern it encourages.

Consumers who customize their Crocs with multiple charms are effectively treating the product as a platform rather than a single purchase.

This reinforces two dynamics:

Collection behavior - consumers purchase multiple pairs rather than replacing one pair.

Switching friction - abandoning Crocs means abandoning the charm ecosystem attached to those shoes.

These dynamics resemble the accessory ecosystems surrounding products such as Apple devices or gaming consoles. Once a consumer invests in the ecosystem, the probability of switching declines.

For Crocs, Jibbitz helps convert the clog from a one-time purchase into a repeat purchase franchise.

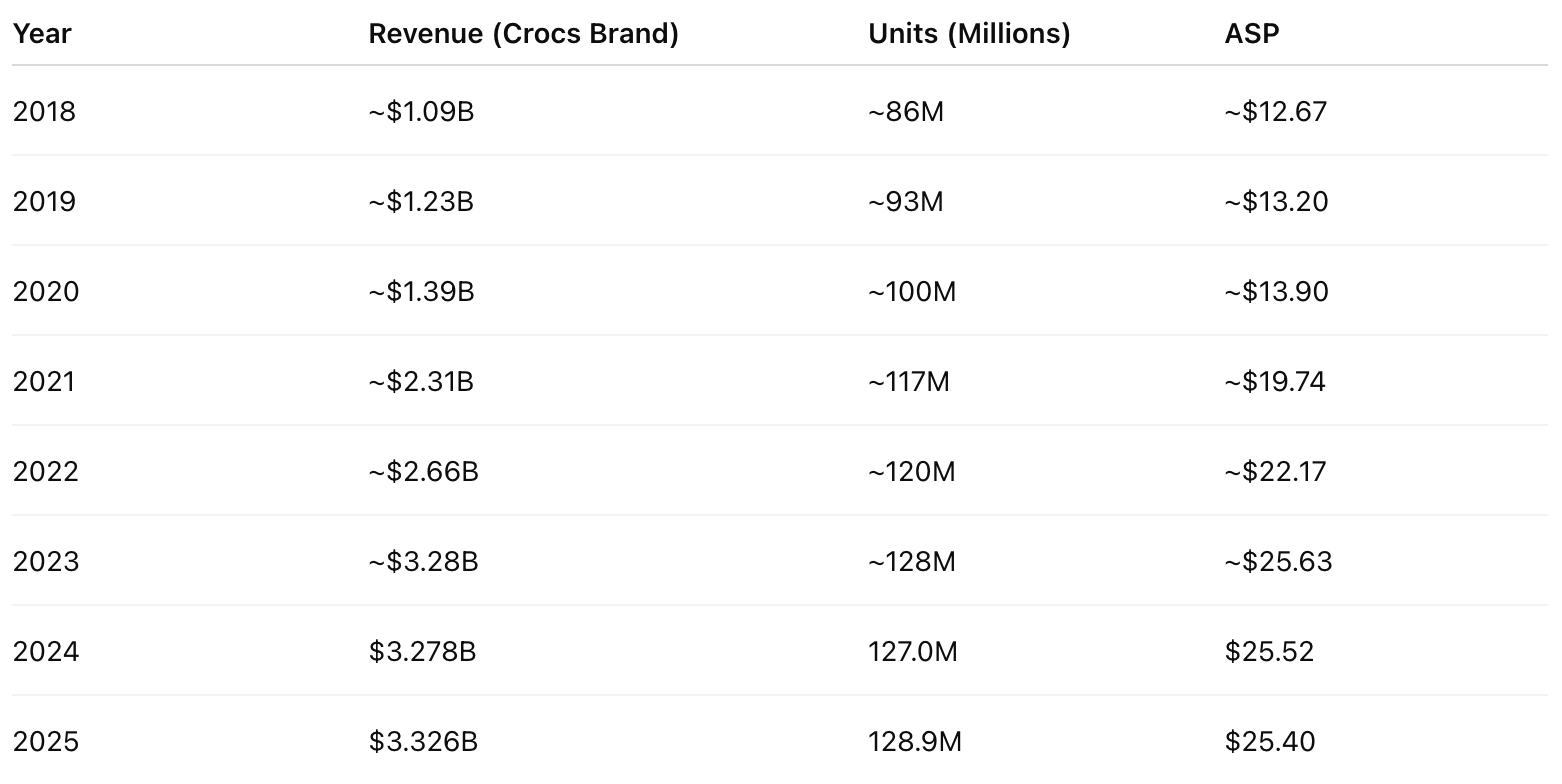

A Note on ASP

One current warning signal deserves acknowledgement.

Crocs Brand ASP declined slightly in FY2024/2025:

Management attributed the decline to increased discounting.

This is an early warning signal but not yet evidence of a structural problem.

To stress-test the thesis, we can examine the impact of sustained ASP decline.

Stress Case: ASP declines 4% annually for 3 years

Revenue impact (holding units constant):

$3.33B x (0.96)^3 = $2.95B

Assuming operating margin compresses modestly to 28%:

EBIT = 2.95B × 28% = 826M

Estimated free cash flow:

~$550M

Even under this scenario the business still generates substantial free cash flow.

At current market capitalization (~$4.5B), the FCF yield remains roughly 12%, preserving the buyback-driven compounding mechanism.

Global Penetration

The global penetration estimate in the thesis is necessarily approximate but can be triangulated from available data.

Crocs has sold over 1 billion pairs globally since inception.

Assuming an average consumer owns 2–3 pairs and replaces them every 3–4 years, the active installed base likely falls between:

200–250M households globally

The addressable household estimate derives from:

global household count (~2.1B)

filtering for middle-income consumers with discretionary footwear purchasing power

This yields roughly 800–900M addressable households.

These figures imply current penetration of approximately:

25–30% globally

North America appears significantly higher than this, while emerging markets remain earlier in the adoption curve.

Recent revenue trends support this interpretation.

International revenue share increased from:

At the current rate of roughly 370 basis points of mix shift annually, international should exceed 50% of Crocs Brand revenue in 2026.

Primary Research: Channel Checks

Public financial statements reveal what Crocs shipped to retailers, but they do not reveal what actually sold through at the store level. Because wholesale partners typically adjust orders several quarters before changes appear in reported revenue, direct channel feedback is often one of the earliest indicators of brand health.

To supplement the desk-based analysis, conversations were conducted with employees and managers across several footwear retailers in Southwest Florida, including sporting goods and footwear specialty stores that carry Crocs products.

While geographically limited, these discussions provide directional insight into retail channel dynamics.

Three consistent observations emerged.

Floor Space Allocation

None of the retailers contacted indicated plans to reduce Crocs floor space for the upcoming season. Store managers described Crocs as a stable category performer, maintaining roughly the same physical footprint within their footwear sections as in prior years.

In consumer brands experiencing channel fatigue, the earliest signal is often floor space contraction, where retailers reduce a brand from multiple display bays to a smaller footprint. No such adjustments were reported.

Sales Trends

Retail staff described Crocs sales as steady rather than accelerating, which is consistent with the stagnation scenario modeled in the valuation framework.

However, the brand continues to generate reliable turnover, particularly in the core clog product line.

One store manager summarized the pattern succinctly: Crocs are not a trend item anymore - they are a permanent comfort shoe category.

Customer Segmentation

Two distinct customer groups continue to drive sales:

Children and teenagers purchasing Crocs as casual footwear, often alongside Jibbitz charms.

Adults purchasing comfort footwear, particularly for everyday use around the home or outdoors.

In several locations, employees noted that Crocs remain especially popular with younger consumers purchasing multiple color variations.

Competitive Observations

The only category where Crocs was reported to be losing some share was within orthopedic or posture-oriented footwear, particularly brands such as OOFOS and similar recovery-style sandals.

However, this competition appeared concentrated among older, wealthier consumers seeking specialized comfort products rather than within Crocs’ core casual footwear segment.

Importantly, retailers did not describe Crocs losing share to direct foam clog competitors at meaningful scale.

Channel Interpretation

These observations are consistent with a stabilizing brand rather than a declining one.

Three conclusions follow:

No evidence of channel fatigue

Retailers are not reducing Crocs floor space.Demand appears steady rather than accelerating

This aligns with the thesis that Crocs is transitioning from a high-growth brand to a mature franchise.Competition is emerging primarily in adjacent categories

Recovery footwear brands are attracting some older consumers but do not appear to threaten Crocs’ core casual footwear segment.

These findings are necessarily limited by geography, but they provide directional confirmation that Crocs continues to function as a reliable footwear category rather than a fading fashion trend.

Future research should include channel checks in additional regions and international markets, particularly China, India, and Southeast Asia, where the long-term growth thesis relies on continued adoption.

Category Fatigue vs Fashion Fatigue

Two risks must be distinguished.

1. Fashion Fatigue

Consumers stop buying Crocs but switch to other footwear brands.

2. Category Fatigue

Consumers abandon foam clogs entirely.

The monitoring signal differs.

If casual buyers decline but professional buyers remain stable, the brand is experiencing fashion fatigue.

If professional buyers decline as well, the category itself may be weakening.

Buyback Compounding: The Core Engine

Crocs generated approximately $659M free cash flow in FY2025.

At current prices this represents roughly 16% free cash flow yield.

Share Repurchases

$577M repurchased in FY2025

Share count reduction: 11%

Explicit Buyback Math

Assuming:

$650M annual free cash flow

$83 share price

9% annual share reduction

Share count falls:

50M → ~32M shares in five years

Per-share free cash flow increases:

$13.10 → ~$20.50

This represents a 57% increase in per-share value with zero growth and zero multiple expansion.

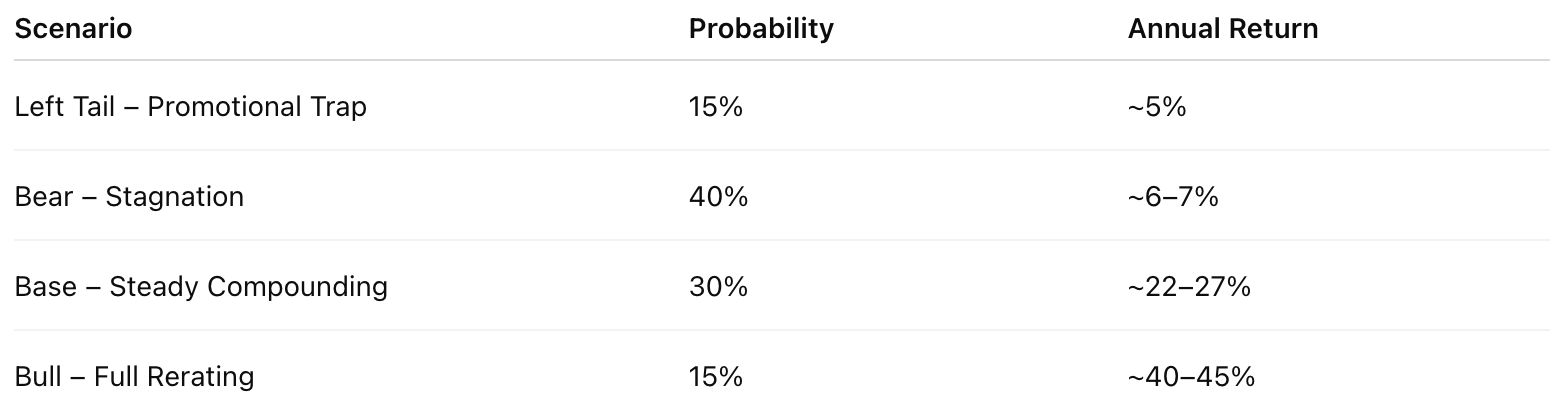

Scenario Analysis (2026 → 2031)

Probability-weighted expected return:

~18–20% annually

The probability distribution presented in the scenario analysis is judgmental rather than statistical. However, the weights reflect observable features of the business and the historical behavior of consumer brands.

The logic behind the probabilities is as follows:

Left Tail – Promotional Trap (15%)

This scenario requires a specific sequence:

sustained discounting

margin compression

eventual unit decline

Historically this process takes 18–24 months to develop. Current data shows early signals (ASP decline) but not the full pattern.

For that reason, a 15% probability reflects that the risk is real but not currently confirmed.

Bear Case – Stagnation (40%)

Stagnation is the most common outcome for consumer brands after their peak growth cycle.

Examples include:

Skechers

Coach

Under Armour

These companies often trade between 7–9× EBIT for extended periods despite stable revenues.

Because stagnation is the base rate outcome for mature brands, the bear case receives the largest probability weight (40%).

Base Case – Stable Compounding (30%)

The base case requires two variables working simultaneously:

international growth offsetting North American maturity

operating margins remaining above ~28%

Each individually has reasonable probability. Their combination reduces the probability to ~30%.

Bull Case – Clean Rerating (15%)

The bull case requires multiple favorable developments:

HD divestiture or stabilization

sustained international expansion

institutional re-rating of the Crocs Brand

Because this outcome requires several variables to align simultaneously, it receives a lower probability weight.

Why the Bear Case Still Works

The bear case falls below our 15% hurdle rate individually.

However, the asymmetry remains attractive.

Even when the thesis partially fails:

capital is preserved

free cash flow remains positive

buybacks continue compounding per-share value

HD Resolution Scenarios

Three outcomes exist.

1. Stabilization

HD remains a drag but manageable.

2. Divestiture

HD sold for ~$800M–$1B, potentially triggering a rerating.

3. Additional Impairment

Another write-down occurs in 2026.

Non-cash but extends negative headlines.

The thesis works under all three scenarios.

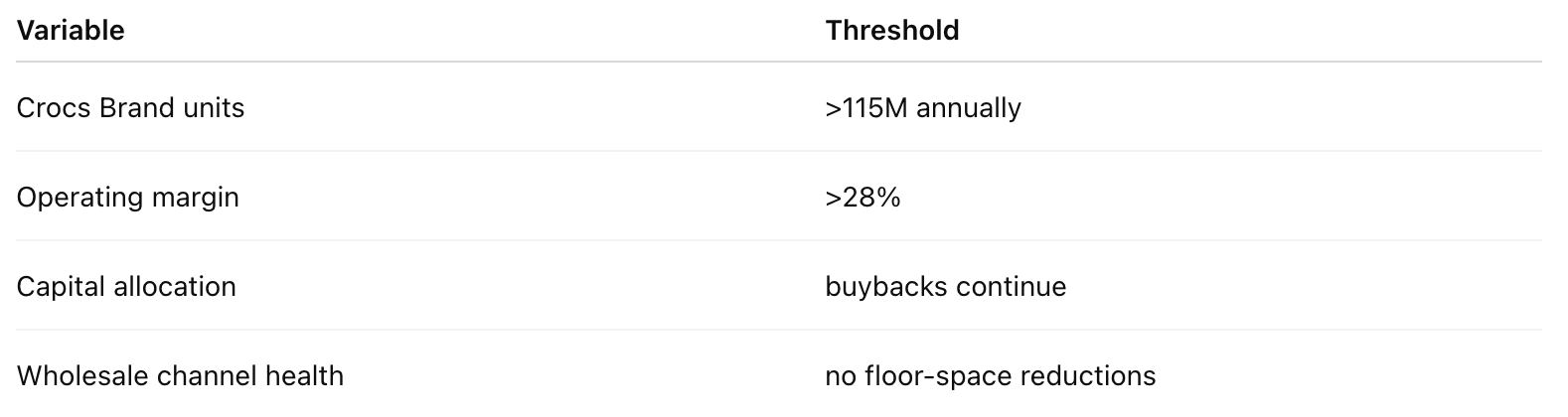

Monitoring Variables

Two variables breaking simultaneously signals thesis failure.

Capital Allocation Discipline

A clear tripwire exists.

Any acquisition above ~$300–400M before HD is resolved would trigger exit.

Conclusion

Crocs today represents a rare situation where a profitable global consumer franchise trades at a valuation normally reserved for structurally impaired and declining businesses.

The Crocs Brand generates roughly $650–750M of annual free cash flow, operates with 60%+ gross margins, and requires very little capital to sustain its business. At the current valuation, that cash flow equates to a ~16% free cash flow yield, allowing the company to repurchase approximately 8–10% of its shares annually at current prices.

This dynamic fundamentally changes the nature of the investment.

The thesis does not require revenue growth, margin expansion, or a multiple re-rating to produce acceptable returns. Even if Crocs never trades at a higher valuation, the buyback program alone compounds per-share value steadily over time. A business producing hundreds of millions of dollars of free cash flow while reducing its share count by high single digits annually will increase intrinsic value per share almost mechanically.

Under conservative assumptions - stable unit demand around 115–120M pairs annually and operating margins above roughly 28% - Crocs should continue generating substantial free cash flow. In that scenario, the most likely outcome is not failure but slow compounding, driven primarily by buybacks.

The upside scenarios arise if one or more additional factors occur:

international markets continue expanding penetration

margins remain near current levels

HD is divested or stabilized, making the Crocs Brand economics clearer to institutional investors

These outcomes would allow the business to compound more rapidly and potentially lead to a higher valuation multiple.

The key point is that the investment does not depend on those outcomes. The core economics of the Crocs Brand already support meaningful value creation.

The true thesis risk is not a fashion cycle or temporary discounting. The real risk would be structural brand deterioration - a scenario in which unit demand falls materially and margins compress simultaneously. That outcome would likely be visible through declining unit volumes, shrinking wholesale floor space, or sustained margin compression below the monitoring thresholds outlined earlier.

Absent those signals, the business should continue producing large amounts of free cash flow and shrinking its share count over time.

At current prices, Crocs does not require the market to recognize its value in order for the investment to work.

The buyback program compounds value quietly while investors wait.

Disclaimer

This memo reflects my personal investment framework and opinions. It is not investment advice. I may be wrong, and circumstances can change. I reserve the right to change my mind as new facts emerge.

| A guest post by

|