FICO: The Benchmark Moat, the Price War, and Why the Stock May Finally Be Fairly Priced

FICO’s moat remains intact - but future returns now depend on how the mortgage pricing battle unfolds.

Executive Summary

Fair Isaac (FICO) is one of the highest-quality financial infrastructure businesses in public markets.

Its moat is not merely an algorithm. Its moat is that the entire credit ecosystem still speaks the language of FICO scores.

Benchmarks embedded across lenders, securitization desks, mortgage insurers, investors, and regulators are extraordinarily difficult to displace.

The recent selloff - triggered by aggressive VantageScore price cuts - forced the market to confront a question it had long ignored:

What happens if FICO’s pricing power in mortgage finally faces real competition?

The answer is more nuanced than either the bulls or bears suggest.

VantageScore introduces real competitive pressure, but the economics of the mortgage ecosystem suggest the actual financial incentive to switch is extremely small.

At roughly $1,155, FICO is no longer obviously expensive. It is entering the range where an investor can plausibly underwrite 10–12% annual compounding if the benchmark survives and the company executes on its Direct License strategy.

That is not the same thing as saying the stock offers a margin of safety. It does not. But it may now represent a rational entry point, or a starter position, for investors who believe in the durability of the franchise.

What FICO Actually Is

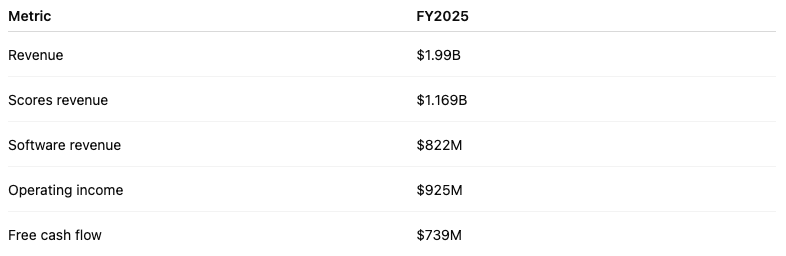

FICO reported fiscal 2025 revenue of approximately:

The company operates two businesses.

1. Scores (the economic engine)

Scores produced approximately $677M of operating income in fiscal 2025.

That represents roughly 73% of total operating income, despite representing about 59% of total revenue.

Segment margins are extremely high - about 88% operating margin - which means incremental score revenue flows disproportionately to the bottom line.

This segment remains the primary driver of FICO’s economics and moat.

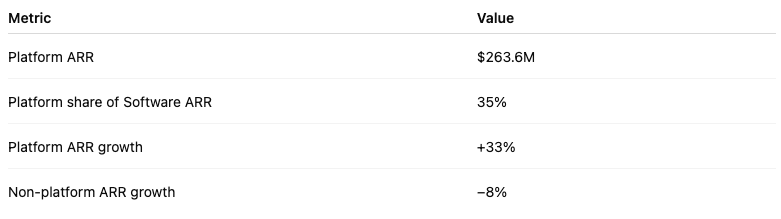

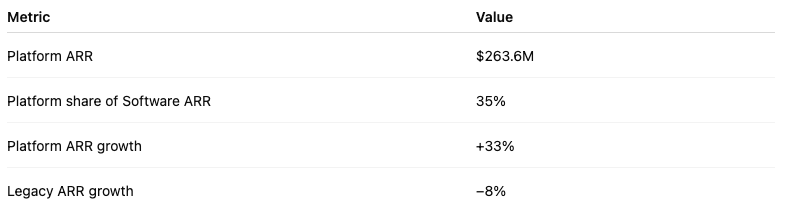

2. Software (important but secondary)

Software generated about $247.7M of operating income, or roughly 26–27% of company-wide operating income.

The segment currently operates around 30% margin and is best understood as a mix-shift story.

Key metrics:

The key question for Software is whether the rapidly growing FICO Platform becomes dominant in the mix over time. If that happens, segment margins could expand materially. If not, Software remains a useful but secondary driver of value.

The Real Moat: Benchmark Status

Most commentary about FICO misidentifies the moat.

The moat is not underwriting accuracy.

Many lenders use proprietary underwriting models.

The real moat is that FICO functions as the benchmark language of credit risk.

Participants that rely on this benchmark include:

mortgage lenders

securitization investors

mortgage insurers

warehouse lenders

regulators

capital markets desks

Even lenders that do not rely on FICO internally often disclose average FICO scores when selling loan pools.

That places FICO closer to businesses like:

Moody’s ratings

MSCI indexes

S&P benchmarks

Bloomberg terminals

Benchmarks become deeply embedded across ecosystems. Replacing them requires coordination across many stakeholders simultaneously.

That is extraordinarily rare.

Why VantageScore Has Struggled for Two Decades

VantageScore has existed since 2006.

It has often been cheaper than FICO.

Yet it has failed to displace FICO in mortgage.

The reason is ecosystem inertia.

Mortgage finance relies on:

securitization performance models

mortgage insurance underwriting

investor reporting frameworks

regulatory disclosures

All of these have been built around FICO score distributions.

The real change in 2025 was regulatory.

FHFA allowed lenders to choose between Classic FICO and VantageScore 4.0 for Enterprise loans while stating that current credit reporting requirements would not initially change.

That opened the door to competition.

But regulatory permission does not automatically create adoption.

The Basis-Point Reality

The most useful way to evaluate the VantageScore price war is to convert the pricing differences into basis points of mortgage principal.

Assume:

one borrower

tri-merge remains in place

three score pulls during the mortgage process

Approximate economics:

On a $300,000 mortgage

On a $500,000 mortgage

This is the key insight.

The price difference is economically tiny relative to the overall mortgage transaction.

Even the largest difference is under 5 basis points of loan value.

The Hidden Moat

FICO is the default language of the securitized credit market.

One of the most underappreciated parts of the FICO moat does not sit at the point where a loan is approved. It sits at the point where the loan is sold.

Mortgage lenders rarely hold loans on their balance sheets for long. Instead, they originate loans and sell them into the secondary market, where they are pooled into mortgage-backed securities and purchased by institutional investors.

In that system, investors need a standardized way to evaluate credit quality across thousands of loans.

That standard has historically been the FICO score.

For decades, mortgage pools sold to investors have been described using metrics such as:

weighted average coupon

loan-to-value ratios

geographic distribution

delinquency history

average FICO score

FICO score distributions have become a shorthand language for credit risk.

Institutional investors, mortgage insurers, and securitization desks have built decades of performance models around these score bands. Historical default rates, prepayment behavior, and loss severity assumptions are all tied to FICO ranges.

Replacing that benchmark is not simply a matter of choosing a cheaper score. It requires rebuilding a large body of historical credit performance analysis.

Why a Few Basis Points in Score Pricing Is Economically Irrelevant

The recent VantageScore price war makes this dynamic clearer.

Using realistic mortgage workflow assumptions, the difference between VantageScore and FICO often amounts to only 1–4 basis points of loan value.

For example, switching from FICO to VantageScore might save roughly $35–$80 per mortgage depending on the workflow.

On a $300,000 mortgage, that is roughly 1–3 basis points.

That saving may appear meaningful when viewed as a line item in the underwriting process. But it becomes trivial when viewed in the context of the securitization market.

Consider a $100 million pool of mortgages sold to investors.

If investors require even 10 basis points of additional yield because the credit benchmark is unfamiliar or less trusted, the economics shift dramatically.

Ten basis points on a $100 million mortgage pool equals:

$100,000 per year in additional interest cost

Over the life of the security, that difference can easily reach millions of dollars.

In other words, saving a few thousand dollars in scoring costs can easily be outweighed by a much larger increase in funding costs.

That is why institutional investors tend to prefer established benchmarks even when alternatives are cheaper.

The Rating Agency Analogy

This dynamic closely resembles the role of credit rating agencies.

A company issuing bonds could theoretically save money by using a lesser-known rating firm instead of Moody’s or S&P.

But if investors trust those ratings less, they demand a higher yield.

The cost of capital rises and the savings disappear.

As a result, issuers continue to rely on established rating agencies even when cheaper alternatives exist.

FICO’s position in consumer credit markets is similar.

It is not simply a scoring tool. It is a reference standard embedded in the credit ecosystem.

Why This Matters for the VantageScore Debate

The recent price cuts from the credit bureaus aim to drive adoption by making VantageScore dramatically cheaper.

But the mortgage ecosystem does not optimize for the cost of credit scores alone.

It optimizes for the total economics of selling the loan.

Those economics depend heavily on:

investor confidence

securitization pricing

capital requirements

liquidity in secondary markets

If using a different scoring benchmark increases uncertainty even slightly, the cost of capital rises.

That increase can easily dwarf the savings from lower scoring fees.

Implication for FICO

This dynamic is the core reason the FICO moat has persisted for more than two decades.

Price competition alone has not been enough to displace the benchmark.

The real question for investors is not whether lenders can use VantageScore.

It is whether the entire mortgage ecosystem - investors, insurers, securitization desks, and regulators - is willing to adopt it as the new standard.

Until that happens, the economic advantage of switching away from FICO remains limited.

And as long as FICO remains the dominant benchmark language of credit risk, its pricing power and economic position remain unusually resilient.

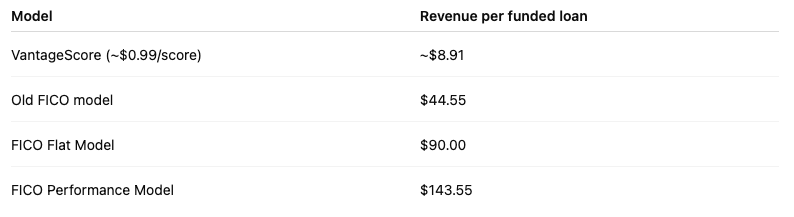

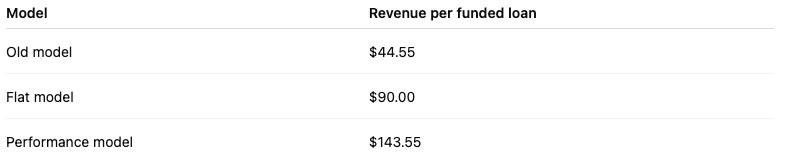

The Direct License Program

Historically, mortgage scoring economics flowed through bureaus and resellers before reaching FICO.

The Direct License program introduces two pricing structures:

Using a one-borrower, tri-merge, three-pull example:

Two key takeaways:

The flat model alone doubles FICO’s mortgage economics.

The performance model increases them by over 3X

The bull case therefore does not require widespread adoption of the performance model.

Software: A Mix-Shift Story

Software is important but not the main reason to own this company.

Key metrics:

If Platform eventually dominates the mix, Software margins could expand meaningfully beyond the current ~30%.

Cyclicality and Multiple Compression

Premium multiple compounders reprice aggressively when uncertainty increases.

Earlier this year, FICO traded near 50× free cash flow.

Today it trades closer to high-30s.

Example using ~$30 FCF/share:

The recent selloff reflects multiple compression faster than moat deterioration.

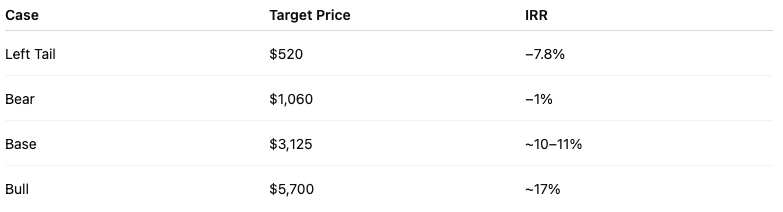

Scenario Framework

From roughly $1,155, the next decade can be framed as:

Bear Case

Assume FCF/share compounds from $30 → $48 (~5% CAGR).

Apply 23× FCF multiple.

48 × 23 ≈ $1,100

From $1,155 this produces roughly −1% annualized return.

Base Case

Assume FCF/share compounds from $30 → ~$92 (~12% CAGR).

Apply 34× FCF multiple.

92 × 34 ≈ $3,125

This produces roughly 10–11% annualized returns.

Bull Case

Assume FCF/share compounds from $30 → ~$143 (~17% CAGR).

Apply 40× FCF multiple.

143 × 40 ≈ $5,700

This produces roughly 17% annualized returns.

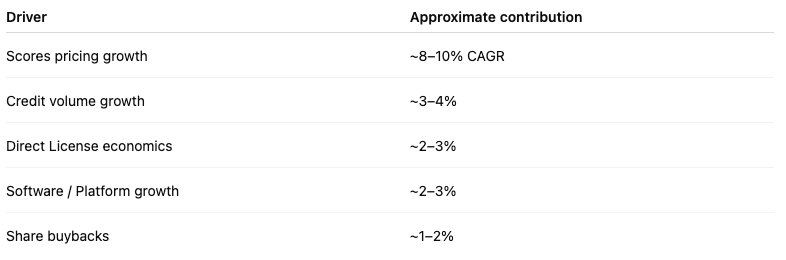

How FCF Could Reach $143 per Share

An LP or institutional reader may reasonably ask how FCF/share could grow from $30 to ~$143 over a decade.

A plausible path looks like this:

Combined, these drivers produce roughly 16–18% FCF/share growth, which over 10 years turns $30 into roughly:

$30 × (1.17^10) ≈ $143

This is aggressive but not unrealistic if:

mortgage economics improve through Direct License

FICO retains benchmark status

buybacks continue at historical pace

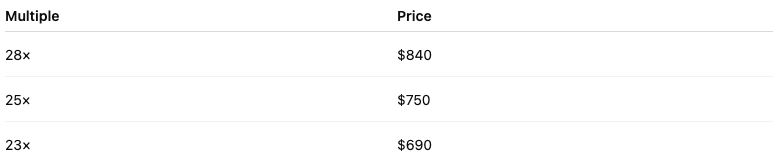

Entry Zones

Margin-of-Safety Zone

Derived from 23–28× FCF multiples.

Margin-of-safety range:

$700–850

Fair-Price Zone

$1,100–1,300

At this range investors may plausibly underwrite 10–12% long-term returns.

Optionality: FICO Score 10T

One upside factor not included in the base valuation is FICO Score 10T, the company’s next-generation scoring model incorporating trended credit data.

If adopted broadly in mortgage, it could:

justify higher pricing

reinforce the benchmark moat

provide another pricing reset opportunity

This represents upside optionality not embedded in the base case.

Final Conclusion

FICO remains one of the strongest benchmark franchises in financial infrastructure.

The VantageScore price war raises legitimate questions about mortgage pricing power but does not automatically break the moat.

The Direct License program meaningfully improves mortgage economics even without perfect adoption.

At roughly $1,155, the stock appears to have moved into a range where a patient investor can plausibly earn 10–12% long-term compounding from a still-dominant benchmark franchise.

This is not a deep value opportunity.

It is a quality compounder purchased at a fair price.

Disclaimer

The information provided in this article is for informational and educational purposes only and reflects my personal opinions. It should not be construed as investment advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own independent research. Any views expressed are subject to change without notice. I may hold positions in the securities discussed and may buy or sell such securities at any time without updating this publication. Investing involves risk, including the possible loss of principal. I assume no liability for any investment decisions made based on the information presented here.

| A guest post by

|