Franklin Covey (FC): Anticipated Future Returns

A probability-weighted framework for sizing risk, not telling stories.

One of the mistakes I’ve made repeatedly as an investor - even while thinking I was doing the “right” work - is this:

I spent enormous time understanding what a business is, why it’s misunderstood, and why it might be cheap, but far less time explicitly modeling what I expect to earn if I’m right… and what happens if I’m wrong.

That gap feels small in the moment. It isn’t.

Without a clear view of expected returns - across good outcomes, mediocre ones, and disappointing ones - capital allocation becomes guesswork dressed up as analysis. Position sizing becomes emotional. Conviction becomes narrative-driven. And patience becomes much harder to maintain when the stock moves up or down.

This post is less about Franklin Covey than it is about correcting that mistake - for myself first. It’s the kind of note I want to reread years from now, and eventually share with my kids when I start teaching them how value investing actually works in practice, not just in theory.

The Original Thesis (Still True)

The market thinks Franklin Covey is a slow-growth training company.

It isn’t.

Franklin Covey is a subscription-based, global human-performance platform whose economics are obscured by accounting rules that delay revenue recognition by 12–24 months.

Customers buy the All Access Pass (AAP) - a recurring subscription that includes:

Leadership development

Cultural alignment programs

Trust-building frameworks

Execution systems

Coaching, consulting, and digital tools

AI-enabled reinforcement and practice

Conceptually, it’s closer to:

LinkedIn Learning + behavioral consulting + SaaS-like subscriptions + coaching-as-a-service

But with something harder to replicate: 40 years of codified IP (7 Habits, Speed of Trust, 4DX) and deep institutional embedding across Fortune 500 enterprises and more than 8,000 schools.

This isn’t content you read.

It’s content organizations run on.

The Transformation That Created the Mispricing

Over the last decade, Franklin Covey deliberately rebuilt itself around:

Subscription revenue

Multi-year contracts

Recurring services

Digital delivery

Capital-light economics

Today:

Subscription revenue represents the majority of total revenue

Multi-year contracts represent 61% of contracted value

Subscription gross margins approach 100%

Services gross margins run 60-65%

Balance sheet is unlevered with net cash

Business is capital-light and cash generative

In FY25, management made a difficult but necessary decision: they restructured the sales organization.

But why?

In retrospect, the FY22–FY23 surge in expansion revenue appears to have been less durable than it initially looked.

As those expanded contracts entered renewal cycles in FY24–FY25, net expansion slowed materially, pressuring deferred revenue and operating cash flow.

The data tells a clear story (per annual 10-K filings):

Unbilled Differed Revenue (UBDR) peaked at $87M in FY23

Declined to $73M by FY25

This suggests FY22-23 multi-year deals either:

Renewed shorter (2yr → 1yr)

Or didn’t renew at similar contract values

Against that backdrop, management’s decision to restructure the sales organization - moving toward specialization, clearer role separation, and longer-duration contracts - looks less like a growth initiative and more like a necessary correction to improve renewal quality and cash flow durability.

They moved from a generalist model to:

Hunters and farmers

Vertical specialization

Better pipeline management

Higher ACVs

Longer-duration contracts

That transition - compounded by macro uncertainty early in FY25 - did suppress reported results and near-term cash flow.

But critically, this was a self-inflicted, transitional economic reset, not a deterioration in the underlying value of the franchise.

The market priced it as permanent impairment.

That mismatch is the source of the mispricing.

The Accounting Lag (The Real Source of Confusion)

Here’s the key mechanic the market still struggles with:

Cash and contracts grow first.

Reported revenue follows 12–24 months later.

A majority of contracted dollars (61%) are tied to multi-year contracts, which flow like this:

Year 1 → billed upfront → Deferred Revenue

Years 2–3 → contracted but unbilled → Unbilled Deferred Revenue (UBDR)

GAAP revenue → recognized ratably over the contract term as access and services are delivered

That means:

UBDR is the true leading indicator

Deferred revenue is lagging confirmation

GAAP revenue is the last thing to move

UBDR is not “missing revenue” - it’s future contractual revenue awaiting billing, and its durability depends on renewal quality.

This is why FY25 looked weak even as underlying economics stabilized.

It’s also why FY26 will likely look “fine but uninspiring” - while FY27 is already being shaped economically today.

Why This Is NOT Speculation

Speculation bets on unknowns.

This situation does not.

Key indicators through FY25 and into FY26:

New logo activity remained healthy despite the sales transition

Invoiced amounts improved despite a disruptive sales reorganization

Services and coaching penetration increased

Client retention remained stable, with pressure concentrated in expansion rather than logos

Deferred revenue continued to grow

UBDR stabilized after the renewal cycle

Leading indicators in Q1 FY26 improved meaningfully.

NA invoiced growth: +7% (+13% ex-government)

New logo subscriptions: +25% YoY

Services bookings: +29% YoY

Deferred revenue: +5% YoY to $100.2M

Multi-year contract mix: 61% of contracted value (stable)

If Franklin Covey had lost relevance or market share, these indicators would not be improving.

This was not a loss of relevance or demand - it was an execution and timing problem.

That distinction matters.

What became clear to me as I worked through Franklin Covey wasn’t just something about the business itself - it was something about my own process.

I was comfortable saying the reported weakness came from execution and timing rather than a broken model. I was comfortable saying the economics were real but delayed. What I wasn’t yet doing was forcing myself to fully translate that view into explicit outcomes and probabilities.

That’s where I had to slow down.

Up until now, I’ve typically framed investments using three scenarios: bull, base, and bear. It’s a useful shorthand, and it’s how I’ve approached most opportunities in the past. But as I dug deeper into Franklin Covey, I realized that framework can blur an important distinction.

In practice, what we casually call a “bear case” often combines two very different realities:

situations where the business works, but returns disappoint

and situations where capital is impaired even though nothing collapses

Those outcomes may sit next to each other in a spreadsheet, but they demand very different position sizing, patience, and risk management.

So rather than abandoning the old framework, I refined it. For the first time, I explicitly modeled four outcomes instead of three, separating out a true left tail - not because it’s likely, but because pretending it doesn’t exist makes sizing decisions harder than they need to be.

This is the framework I’ll use going forward.

The Four Scenarios (2-3 Year General)

Starting point:

Stock price: $19

Shares outstanding (pre-buybacks): ~11.9M

Net cash: ~$20M

$20M buyback authorization (~10% of shares)

1. Left Tail: Capital Impairment (≈10%)

Nothing blows up.

There’s no fraud.

No leverage.

No bankruptcy.

But execution remains weak, working capital never normalizes, and renewals shorten.

Assumptions (FY27):

EBITDA stagnates: ~$28–29M

FCF conversion: ~55–60%

FCF: ~$15–18M

Buybacks: only the $20M authorization

Shares: ~10.8M

Market multiple: ~9× FCF

Outcome:

Equity value ≈ $150–165M

Stock price: ~$15–17

This is the Type-1 error I am trying to avoid.

Note: This is not bankruptcy or collapse. This is chronic weak execution with working capital issues that persist. No fraud, no leverage, no secular obsolescence - just a business that doesn't work well enough.

2. Bear: Stall / No Re-Rate (≈30%)

The business works - but not well enough.

Assumptions (FY27):

EBITDA grows modestly: ~$32–33M

FCF conversion: ~68%

FCF: ~$22M

Buybacks slow after authorization

Shares: ~10.5M

Market multiple: ~10× FCF

Outcome:

Equity value ≈ $230–240M

Stock price: ~$22–23

You don’t lose much.

You don’t get paid.

This is the most dangerous outcome psychologically.

3. Base Case: Slow Normalization (≈40%)

Execution improves gradually.

Assumptions (FY27):

EBITDA: ~$36–38M

FCF conversion: ~70–72%

FCF: ~$25–27M

Buybacks continue modestly

Shares: ~9.9–10.0M

Market multiple: ~13× FCF

Outcome:

Equity value ≈ $350–380M

Stock price: ~$30–36

This is a solid, respectable outcome.

4. Bull Case: Bow Wave Releases (≈20%)

Everything lines up.

Assumptions (FY27):

EBITDA: ~$45–50M

FCF conversion: ~72–75%

FCF: ~$30–35M

Aggressive buybacks funded by cash

Shares: ~9.4–9.6M

Market multiple: ~15× FCF

Outcome:

Equity value ≈ $450–520M

Stock price: ~$45–55

This is the asymmetry - but it must be earned.

Probability-Weighted Expected Returns

Expected return from $19: ~+78%

Expected IRR (~3 years): ~20–22%

That return profile is attractive, but it comes with real uncertainty - including a meaningful probability of underwhelming outcomes and a smaller, but non-trivial, risk of capital impairment.

Translating Expected Returns into Intrinsic Value

Rather than treating probability-weighted outcomes as something to discount again, I found it more useful to ask a simpler question:

What does the market appear to be assuming today?

At roughly $19 per share, Franklin Covey is being valued somewhere between my stall and base scenarios. In effect, the market seems to be pricing in a meaningful chance that execution fails to improve materially, that free cash flow conversion remains inconsistent, and that the business never earns a durable re-rating.

That skepticism is understandable. It reflects recent execution scars and the reality that accounting recognition still lags the underlying economics.

What My Work Suggests Instead

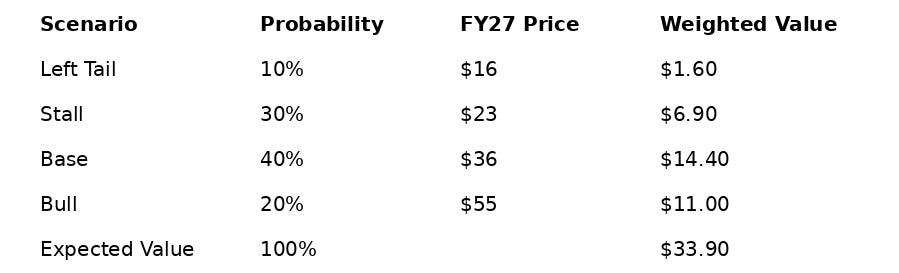

After explicitly modeling four outcomes - including a true left tail - my own probability-weighted view looks different:

roughly 60% probability of base-or-better outcomes (>$30 per share),

about 30% probability of a stall outcome (~$23 per share), and

approximately 10% probability of capital impairment (~$16 per share).

Weighting those outcomes produces an expected value of approximately $33–34 per share in 2–3 years, compared with a current price of ~$19.

That gap does NOT represent certainty. It represents potential alpha - if my probabilities are closer to reality than the market’s.

Viewed through that lens, buying Franklin Covey at ~$19 implies an expected annual return of roughly 20–22%, over three years, driven not by heroic assumptions, but by modest execution improvement, normalization of cash-flow conversion, and rational capital allocation through buybacks.

What This Means for Positioning

There remains a real probability of underwhelming outcomes, and a smaller but meaningful probability of capital impairment without collapse. Because of that, this is NOT a situation that justifies aggressive sizing today.

Franklin Covey earns a starter position, not blind conviction.

Capital is best reserved and scaled only as the data - particularly free cash flow conversion - proves the thesis rather than the narrative.

This is how patience becomes discipline instead of paralysis.

The Lesson I’m Taking Forward

The most important takeaway here isn’t about Franklin Covey.

It’s this:

I don’t think I can allocate capital well without explicitly modeling expected returns and their probabilities.

A great business can still be a poor investment.

A misunderstood company can still disappoint.

And conviction without probabilistic thinking is just storytelling.

This post is me correcting that - in public - so I don’t forget it later.

Franklin Covey remains on the front edge of my radar.

The economics are real.

The accounting lag is undeniable.

The upside exists.

But execution stories must be validated, not assumed.

So for now:

I watch closely

I verify relentlessly

I let the data prove it

If I ultimately add more, it won’t be because the narrative improved.

It will be because the expected returns earned the right to size.

Disclaimer

This memo reflects my personal investment framework and opinions. It is not investment advice. I may be wrong, and circumstances can change. I reserve the right to change my mind as new facts emerge.

| A guest post by

|