GigaCloud (GCT): Anticipated Future Returns

And the Decision to Hold or Add...

Why this memo exists

This memo exists for one reason:

To anchor my thinking about GigaCloud Technologies (GCT) to first principles, not price, headlines, or quarterly noise.

I will reread this before earnings, before adding, and before selling.

If my future actions contradict what’s written here, I should be able to point to new facts, not emotions.

My entry: acknowledging the advantage I already have

I began buying GCT at an average price of $17.98 per share.

At the time:

Enterprise value was roughly $800M

Unlevered free cash flow (UFCF) implied a ~14% yield

The business was priced like a low-quality logistics operator

The market was ignoring the emerging 3P marketplace + logistics flywheel

I was effectively buying:

a profitable, capital-light business, debt free

with real cash generation

at ~7× UFCF

The subsequent re-rating to ~$40/share was not luck - it was the market correcting a misclassification.

That advantage exists only once.

The decision today is not “was I right?”

It is:

At ~$40/share (~$1.6B EV), does GCT still offer attractive forward returns?

What kind of business GCT actually is

GCT is not:

a pure marketplace

a pure logistics company

a pure distributor

It is a hybrid, logistics-first marketplace, and that order matters.

For decades, GCT operated as a 1P business, learning how to:

move bulky goods

manage fulfillment density

control last-mile delivery

operate warehouses profitably

Only in 2019 did the 3P marketplace emerge.

This matters because:

Most marketplaces struggle to add logistics

GCT added a marketplace on top of logistics that already worked

That inversion is the core competitive advantage.

The economic model (simplified, on purpose)

I do not model dozens of scenarios.

I model in-variants and bounds.

Economic gross profit today

3P marketplace: ~6% economic take on GMV

1P business: ~29% gross margin

Combined gross profit today is ~$250M

Corporate overhead

After stripping out operational costs embedded in COGS:

True corporate overhead ≈ $100M

This includes executives, finance, legal, core platform engineering

This distinction matters enormously.

Why 1P matters (and why it’s not a crutch)

Today, 1P gross profit still meaningfully supports free cash flow.

That is not a weakness.

It provides:

stability through freight cycles

predictable gross profit

downside protection while 3P scales

Importantly:

Management has not signaled any intent to exit 1P

Inventory continues to be allocated where ROIC makes sense

This is closer to Costco (Kirkland) or Amazon (Amazon Basics) than to a pure marketplace ideology.

The long-term inflection point I am watching is:

When 3P gross profit alone fully covers corporate overhead.

At that point:

1P becomes optional capital allocation

the business qualitatively de-risks

free cash flow convexity increases

Current valuation: what the market is saying

At ~$40/share:

Market cap ≈ $1.5B

Enterprise value ≈ $1.6B

Unlevered FCF ≈ $114M

EV / UFCF ≈ 14×

UFCF yield ≈ 7.1%

A 14× UFCF multiple implies the market believes:

GCT is durable

cash flows will exist

but growth will be modest

and economics will remain logistics-like

This is not a distressed valuation.

It is also not a compounder valuation.

That framing is crucial.

The floor: what has to go wrong to lose money

My floor case assumes:

3P economic take remains ~6%

service margins do not recover meaningfully (~12% today)

1P margins compress slightly but remain profitable (29% → 27%)

corporate overhead grows conservatively to ~$150M over a decade

no multiple expansion

no buybacks

Even under those assumptions:

UFCF remains roughly flat to modestly growing

shareholder returns land around 7–9% annually

This is the bond-like floor.

Permanent capital loss would require:

structural failure of logistics economics

loss of seller ROI

or severe capital misallocation

I do not see evidence of that today.

The base case: why this is still attractive

My base case requires favorable but not heroic outcomes.

It assumes:

long term 3P GMV growth in the mid-teens

long term 1P GMV growth in the high single digits

3P economic take stays flat at ~6%

1P gross margin stays ~27–29%

corporate overhead growing slower than GP (~4%)

no dramatic margin expansion

Under this framework:

UFCF compounds in the high single digits

combined with a 7% starting yield

total returns reach ~12–15% without multiple expansion or share buybacks

That is a solid outcome for a business with bounded downside.

The upside case: where returns become asymmetric

The upside is not driven by valuation.

It is driven by economics.

If:

3P GMV sustains 18–20% growth (again, 24% YoY LY)

1P grows 5–7% (again, 34% YoY LY)

blended gross profit compounds at ~12%

corporate overhead remains disciplined (~$140–150M)

Then over a decade:

gross profit approaches $800M

EBIT approaches $650M

Unlevered free cash flow approaches $450M

At that point:

even a conservative multiple implies substantial upside

returns reach the high-teens to low-20s IRR

This scenario does not require:

Amazon-level margins

advertising

SaaS miracles

It requires:

logistics density

seller ROI

and time

Buybacks: the quiet return accelerator

There is $95M remaining share repurchase authorization, roughly 6% of shares outstanding.

Larry Wu has demonstrated:

opportunistic repurchases

willingness to step in during volatility

owner-like capital allocation

At today’s valuation:

buybacks (if continued) add 2–3% annualized to per-share returns

without relying on growth or re-rating

This matters more now than it did at $18.

Rather than assuming a fixed annual repurchase rate, I assume GigaCloud has the capacity to retire approximately 4–6% of its share count annually over time when valuation and conditions permit. Over a decade, this translates into a meaningful increase in per-share ownership, even if execution is uneven.

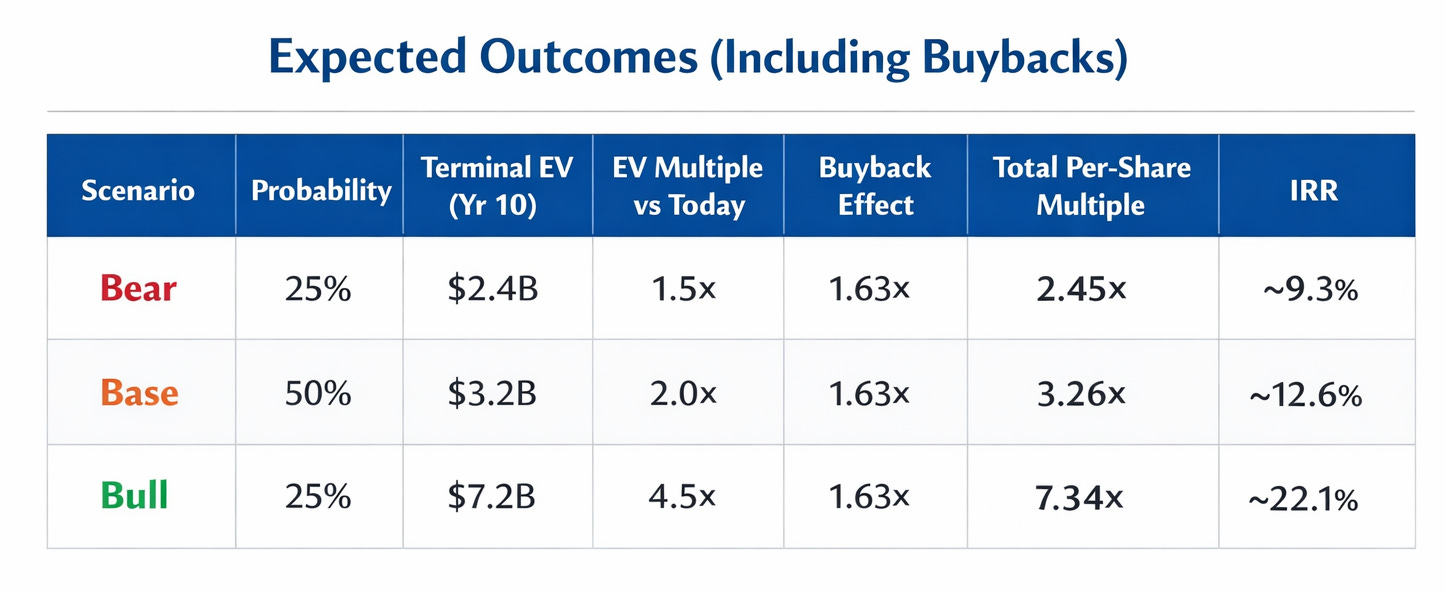

Scenario Table

The decision framework at ~$40

This is no longer a deep value trade.

It is a compounder-with-optionality decision.

Hold: easy yes

downside is bounded

business quality intact

Add modestly:

if 3P growth remains >15%

if corporate overhead stays disciplined

if platform commission continues to creep

Add aggressively:

only on dislocation

or explicit capital return acceleration

I do not need to force action.

What would make this memo wrong

I should reconsider if I see:

Downside Scenario (25% probability):

- 3P economic take: 6% (flat, no recovery)

- 3P GMV growth: 10% CAGR (cohorts underperform)

- Exit multiple: 9x (market remains skeptical)

- 2035 FCF: $200M

- 2035 EV: $1.8B

- Return: 1.2% CAGR + 3% buyback = 4.2% total

This is my “permanent capital loss” threshold.

structural deterioration in seller ROI

persistent overhead bloat

abandonment of capital discipline

evidence that logistics density is not compounding

Absent those, time is working in my favor.

Closing thought

I bought GCT cheaply once.

That opportunity is gone.

What remains is something rarer:

A profitable, founder-led, capital-light business with real cash flow, bounded downside, and credible paths to upside.

At today’s price ($40), using conservative probability-weighted outcomes, I estimate GigaCloud’s intrinsic enterprise value at approximately $4 billion, compared with a current enterprise value of roughly $1.6 billion. In other words, the market is valuing the business at around 40 cents on the dollar of intrinsic value. Importantly, this discount does not presume near-term realization. It reflects a long-term assessment in which intrinsic value compounds steadily, downside outcomes still grow, and ongoing share repurchases increase each remaining owner’s claim on that value. As with all such investments, the timing of convergence is uncertain; however, where value compounds internally and capital is allocated rationally, patience has historically been a sufficient catalyst.

In summary, buying GCT at ~$40 today with a probability-weighted intrinsic value of ~$4.0B, realized over the next decade, with buybacks continuing at ~5% annually, total return on capital will be approximately 15% per year over 10 years.

Disclaimer

This memo reflects my personal investment framework and opinions. It is not investment advice. I may be wrong, and circumstances can change. I reserve the right to change my mind as new facts emerge.

| A guest post by

|

Thank you. Rigourous analysis like this anchors proper valuation.