Goodbye REFI

A record of reasoning. An admission of uncertainty. And, ultimately, an exit.

I’ve spent the last week doing something that feels simultaneously boring and deeply important: reading filings, building a loan-by-loan credit framework, and sitting with uncomfortable probability-weighted truths.

This post is the result.

It’s not a victory lap.

It’s not a prediction.

It’s a decision memo.

A record of reasoning. An admission of uncertainty. And, ultimately, an exit.

Because value investing isn’t about being clever. It’s about not being stupid.

And there is one kind of stupidity Warren Buffett and Charlie Munger spent their entire careers trying to avoid:

Permanent capital loss.

The Setup: Why REFI Was Attractive

Chicago Atlantic Real Estate Finance (REFI) initially looked like a classic “get paid to wait” opportunity, a classic workout:

Stock price in the low to mid $12s

Dividend yield around 15%

Apparent discount to book value

Loan yields in the mid-teens

Conservative reported leverage

Exposure to a hated sector (cannabis), which markets often over-discount

The original thesis was straightforward:

Collect a large dividend while credit fears fade, loans season, and the stock re-rates closer to book.

But credit investing punishes simple narratives.

Because in credit, the risk is not volatility.

The risk is impairment.

So the work had to begin where it always must: at the loan level.

How to Underwrite REFI Properly (A Credit Lens)

REFI is not an equity compounder. It is a credit vehicle. That means it must be underwritten like a lender, not a storyteller.

For each loan, the relevant questions are:

What is the real collateral coverage (real estate LTV, enterprise value)?

Who is the sponsor, and in which jurisdiction?

Is interest paid in cash or PIK?

When does the loan mature, and on what terms can it be extended?

What are the default and covenant triggers?

What is the realistic probability of default?

If default occurs, what is the loss given default (LGD)?

Credit investing is not about asking “what’s the yield?”

It’s about asking “what happens if I’m wrong?”

The Catalyst That Changed the Distribution

By late 2025, a meaningful portion of the REFI loan book was approaching maturity.

By early 2026, several large loans - representing roughly 20%+ of the portfolio - had passed maturity dates.

And yet: no public update.

No press release.

No 8-K.

No portfolio commentary.

This silence did not prove distress. But it changed the distribution of outcomes.

In credit, missing information does not mean neutral risk. It means wider variance.

My IR Inquiry and the CFO’s Response

I contacted investor relations and asked directly what had happened to the matured loans.

The CFO’s response was legally precise and maximally cautious.

Three things it did NOT say:

“Portfolio is performing well.”

“Loans were repaid or extended on favorable terms.”

“We’re pleased with our Q4 results.”

Instead, he gave the most Reg FD-compliant non-answer possible.

That’s what CFOs do when they can’t say anything good but also can’t lie.

This response does NOT confirm distress.

But it does confirm something important:

Management knows the outcomes.

Those outcomes are material enough to be disclosed in the 10-K.

I do not have that information yet.

That is information asymmetry.

And information asymmetry is poison when combined with a large position size in credit.

The Shelf Registration: Optionality, But Context Matters

REFI filed a shelf registration on January 16, 2026.

A shelf registration is not inherently bearish. It’s optionality.

But context matters.

When a REIT files a shelf registration:

Six months after clean earnings → probably routine

Two weeks after large undisclosed maturities → probably defensive

I don’t need proof.

I need probabilities.

And the timing shifted my prior.

Base Rates Matter: Grounding the Probabilities in Reality

At this point, assigning probabilities without base rates would be intellectual theater, and this has been one of my shortcomings in the past.

So I anchored my scenario weights in actual credit base rates, not vibes.

Base-Rate Observations (from specialty lending & CRE credit history)

Late-cycle commercial credit

When large loans mature in stressed environments:~60–70% are extended or refinanced

~30–40% experience some form of distress (modification, non-accrual, or loss)

Cannabis-adjacent lending (higher volatility, weaker refinancing markets)

Higher default frequency than traditional CRE

Lower recovery predictability due to:

regulatory friction

single-tenant properties

sponsor fragility

Observed non-accrual base rate

REFI already had existing non-accruals

Base rates rise meaningfully once non-accruals appear

Credit problems cluster - they do not arrive one-by-one

LGD Modeling: Why the Left Tail Is Real

Loss Given Default (LGD) is where equity holders get hurt.

Even with real estate collateral, cannabis-related loans exhibit:

longer workout timelines

higher carrying costs

fewer natural buyers

higher liquidation discounts

Conservative LGD assumptions for stressed loans:

Best case (clean workout): 20–30% loss

Typical impairment: 40–50% loss

Fire sale / stigma scenario: 60%+ loss

If ~20–25% of the portfolio enters impairment territory, even moderate LGDs translate into:

material book value erosion

dividend impairment

capital raises

and most importantly: ROE compression

That’s how equity gets permanently impaired without bankruptcy.

Why These Base Rates Led to 30 / 50 / 20 Probabilities

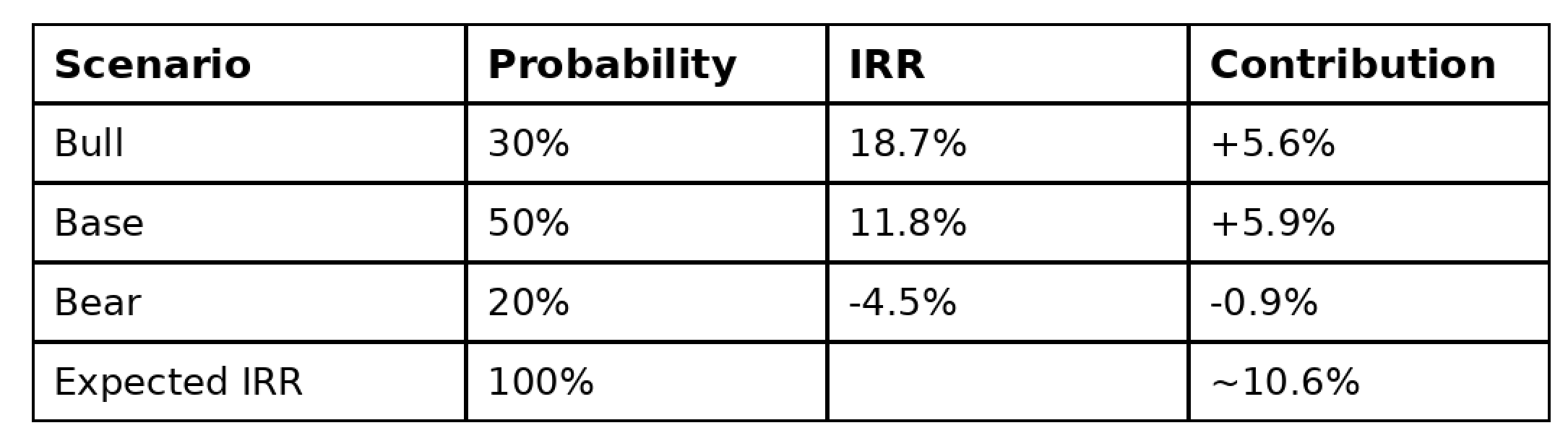

Putting it all together:

30% Bull:

Clean extensions dominate, impairments contained, ROE survives50% Base:

Mixed outcomes - some impairment, and manageable losses20% Bear:

Credit clustering + higher LGDs + capital dependence → stigma and permanent loss

These are not precise. They are reasonable.

And they are consistent with observed outcomes in late-cycle specialty credit.

Expected Return Analysis

Entry price: $12.37 (2/4/26)

Horizon: 3 years

Bull Case - “Clean Extensions, Stability Restored”

Probability: 30%

Book Value Path

Year 1: $14.70

Year 2: $15.30

Year 3: $16.00

Terminal Multiple

~0.92× book

Terminal Price

$16.00 × 0.92 = $14.72

Cash Flows

Dividends: $1.88 × 3 = $5.64

Returns

Total value: $20.36

IRR: ~18.7%

Base Case - “Messy, but Manageable”

Probability: 50%

Dividend Path

Total dividends: $4.88 (small drop)

Book Value Path

Year 3: $14.25

Terminal Multiple

~0.90× book

Terminal Price

$12.83

Returns

Total value: $17.71

IRR: ~11.8%

Bear Case - “Impairment, Dilution, and Stigma”

Probability: 20%

IRR: ~-4.5%

The Bear Case Is Not One Outcome - It’s a Distribution

When I say “bear case ≈ -4.5% IRR,” that is a probability-weighted average, not the worst outcome.

Inside the bear distribution:

40% probability:

Dividend cut + modest dilution → -10% to -15% loss40% probability:

Material impairment + ROE compression → -20% to -30% loss20% probability:

Cascade + stigma + permanent capital loss → -40% to -50% loss

Credit doesn’t fail at the average.

It fails in the tail.

That tail - not the -4.5% average - is what breaks compounding.

Probability-Weighted Expected Return

Call it ~10–11%.

Why That Still Isn’t Good Enough

A ~10–11% expected IRR is not bad.

But expected return only matters after survival is guaranteed.

Buffett said it best:

“I don’t care if something has a higher expected return if it carries a risk of permanent capital loss.”

And Munger was even clearer:

If you’re uncertain, be uncertain with less money.

REFI violates both of my portfolio rules:

Track A (compounders): no long-tail risk allowed.

Track B (workouts): no scenarios involving 30–50% permanent loss.

This is not about whether REFI works.

It’s about what happens if it doesn’t.

What Would Make Me Re-Enter?

I’m not ruling out REFI forever.

But re-entry requires evidence, not hope.

In the 10-K

Non-accruals <15% of portfolio

CECL reserve < $10M

Book value > $13.50/share

Dividend maintained or cut <15%

No equity raise > $30M

In the Following 6 Months

No further non-accruals

Loan maturities handled cleanly

Portfolio growth resumes

Stock trades ≥0.90× book

Final Decision: Why I’m Exiting

I didn’t exit because I know REFI will crash.

I exited because:

I had a large position (10%)

With a -4.5% bear IRR

And a 20% probability of 40–50% permanent loss

Violates my risk budget

Even if REFI works, the position was wrong-sized.

Kelly math is unforgiving:

10% exposure requires >90% conviction

I had 80% at best

The math says sell - regardless of outcome.

Lessons Learned (For My Future Self)

Credit is about survival, not yield.

Missing information widens distributions.

Variance + concentration is how Type I errors happen.

The real bear case is stigma and ROE compression.

When uncertain, be uncertain with less money - or leave the table.

I didn’t exit because I lost capital (I didn’t) or because REFI will fail. I exited because a concentrated position with non-linear tails is incompatible with disciplined compounding.

What Comes Next

I’ll read the 10-K - carefully, like a lender.

If outcomes are clean and durability is restored, I can always re-enter later.

If outcomes are messy, I’ll be grateful I left.

Most importantly, my capital remains available for true fat pitches.

Because investing isn’t about activity.

It’s about patience, selectivity, and living long enough to compound.

Goodbye, REFI.

| A guest post by

|

The newly released 10-K on March 12, 2026 clarified several key uncertainties that originally drove my decision to exit. The loans that matured in December were not defaulted; they were largely amended and extended, including Loan #2 (extended to December 2026), Loan #8 (extended to June 2026 with a 200-bp rate increase), and Loan #18 (extended to December 2026).

These amendments explain the silence that previously concerned me and confirm that the near-term liquidity fears embedded in my earlier scenario analysis did not materialize. In that sense, the market outcome has so far landed between my bull and base cases, rather than the cascading credit event that defined the bear scenario.

However, the filing also revealed genuine credit stress beneath the surface. As of December 31, 2025, four loans totaling roughly $48.8 million were on non-accrual, a substantial increase from the prior year. This represents roughly 12% of the loan portfolio, and those loans no longer contribute interest income. The company also continues to recycle capital aggressively -receiving roughly $40.4 million in repayments while advancing about $51.1 million of new loan capital early in 2026 - indicating the platform remains operational and actively deploying capital.

Taken together, the filing suggests the portfolio is functioning but under stress. The feared maturity cascade did not occur, but credit quality has deteriorated and earnings power may be pressured if non-accrual balances remain elevated or if new loans are originated at lower yields. Importantly, the core reason for my exit remains unchanged: the distribution of outcomes included a meaningful left tail involving dilution, ROE compression, and multi-year capital impairment. Even though the worst scenario has not yet played out, the position size was incompatible with my risk budget and philosophy of concentrated investing without permanent loss risk.