META: Future Anticipated Returns

A 55% ROIC Machine Priced for Competence, Not Panic

I’ve spent the last several weeks underwriting Meta Platforms (META) from the ground up.

This wasn’t about building conviction to buy it.

It was about determining whether I should.

I currently own ~1%.

If the price per share fell to ~$500 without structural impairment, I would allocate 10%.

This memo summarizes the full framework behind that decision.

What Meta Actually Is

Meta is not a social media company.

Meta is:

An algorithmic attention marketplace that converts ~3.6 billion daily users’ time into advertiser value, increasingly powered by AI - with a large but uncertain option on the next computing platform.

Revenue = Users × Time × Ad Load × CPM

User growth is largely saturated in developed markets.

The engine now runs almost entirely on ARPU.

Over the past two years:

~84% of revenue growth came from ARPU

Only ~16% came from user growth

2023→2024 user growth was nearly flat

Meta is no longer a user-growth story.

It is a monetization improvement story.

ARPU: What’s Structural, What Was Temporary

The 2023–2025 recovery had three layered drivers:

Macro ad recovery

ATT signal rebuild

Reels monetization catch-up

Those tailwinds are largely exhausted.

Going forward, ARPU growth likely follows this path:

Years 1–2: 6–7%

Years 3–5: 4–5%

Years 6–10: 3–4% steady-state

Terminal ARPU assumption: 4–5%

This is not heroic.

It assumes AI improves targeting, but with diminishing returns.

The Four Layers of the Ad Machine

ARPU growth does not come from a single lever. It operates in layers:

1. Retrieval (Step Function)

Architectural improvements in candidate generation.

2. Ranking (Diminishing Returns)

Better conversion prediction → higher advertiser bids.

3. Signal Recovery (Mostly Complete)

Rebuilding post-ATT targeting infrastructure.

4. Advertiser Tooling (Early Stage Optionality)

Advantage+, creative AI, business messaging, agentic commerce.

Layer 4 is the only one that could produce nonlinear upside.

But it is not base case.

The Real Risk: Marginal ROIC Compression

Meta’s existing deployed capital (~$158B) earns ~45–55% ROIC.

But the next $160B+ in AI infrastructure likely earns:

10–12% if ARPU holds at 6–7%

6–8% if ARPU settles at 4–5%

This is the classic high-ROIC trap:

Average ROIC is spectacular.

Marginal ROIC may be ordinary.

If capital base doubles while marginal returns compress, long-term compounding moderates.

Maintenance Capex: The Knife Edge

True maintenance capex is likely between:

~$27B (replacement proxy)

~$40–45B (if AI infra is structurally required)

If GPUs economically last 2–3 years rather than 5.5 accounting years, maintenance rises materially.

This is the single biggest modeling variable.

Reality Labs

RL losses are ~$19B annually.

Breakeven likely requires $20B+ revenue.

Probability-weighted 2030 loss ≈ ~$22B.

RL is persistent drag - but not existential.

Optionality: The Five Surfaces

Probability at least one surface exceeds $10B revenue at >20% marginal ROIC by 2030–2032: ~55–60%.

Candidates:

WhatsApp Commerce

Meta AI Assistant

Agentic Commerce

AR Glasses

Llama Enterprise

Meta has historically succeeded at ad adjacencies, not diversification.

Optionality is real - but not base case.

10-Year Underwriting Framework (Price-Only Terminal)

Current normalized EPS ≈ $26.

Left Tail (15%)

EPS CAGR: 3%

Year-10 EPS ≈ $35

18x multiple → $630

Bear (20%)

EPS CAGR: 5%

Year-10 EPS ≈ $42

20x multiple → $840

Base (35%)

EPS CAGR: 7%

Year-10 EPS ≈ $51

22x multiple → $1,122

Bull (20%)

EPS CAGR: 9%

Year-10 EPS ≈ $62

24x multiple → $1,488

Super Bull (10%)

EPS CAGR: 11%

Year-10 EPS ≈ $74

25x multiple → $1,850

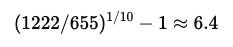

Probability-Weighted Year-10 Value

Expected terminal ≈ $1,222

IRR from $655:

This is price-only IRR.

Buybacks are embedded in EPS growth.

Expected long-term IRR ≈ 6–7%

Not 15%.

Not 12%.

Not even 10%.

Meta at $655 is:

A high-quality business priced near fair value.

Required Entry for 15% IRR

15% over 10 years requires 4.05× capital.

That’s the cold math.

But realistically, with some optionality weighting and shorter horizon:

• $580–600 → ~13% IRR

• ~$540–550 → ~15% IRR (5-year lens)

• ~$500 → strong asymmetric entry

My Decision

At $655:

Expected 10-year IRR ≈ 6–7%

Not mispriced.

Not distressed.

Not compelling at a 15% hurdle.

At ~$500:

You no longer need step-function optionality.

Steady 4–5% ARPU alone likely delivers double-digit IRR.

Downside becomes asymmetrically limited.

I am comfortable waiting.

The Real Insight

This exercise wasn’t about proving Meta is great.

It was about answering:

Do I have edge here?

I don’t have technical edge.

I don’t have informational edge.

My edge is patience during dislocation.

If Meta trades to $500 during recession, AI bust, or regulatory panic - I will size it meaningfully.

Until then:

No forced conviction.

Final Thought

Buffett avoided blue chips in the 1950s because they were priced for competence.

Meta today is priced for competence.

It is not priced for disaster.

The job is not to own every great company.

The job is to own them when price compensates for uncertainty.

I am happy to wait.

Disclaimer

This memo reflects my personal investment framework and opinions. It is not investment advice. I may be wrong, and circumstances can change. I reserve the right to change my mind as new facts emerge.

| A guest post by

|