Visa Inc. (NYSE: V)

Visa (V): One of the Best Businesses in the World - But Is It a Great Investment at today's valuation?

I. Why This Memo Exists

Most investment writing about Visa follows a familiar pattern. It explains the network, highlights the margins, points to the buybacks, acknowledges the litigation, and arrives at the same conclusion: Visa is one of the finest businesses ever built. I largely agree with that assessment. But for a concentrated value investor, that alone is not enough. The real question is simpler and far more important: at today’s price, what return can reasonably be expected over the next decade, what does the range of outcomes actually look like, and is this the best place to allocate capital?

That is what this memo attempts to answer. It is written for the investor who already understands the quality of the business and wants to think clearly about the investment at $323 per share. After working through the scenarios, financials, competitive risks, and long-term assumptions, my conclusion is fairly straightforward: Visa at today’s price is probably a very good investment in an extraordinary business, but not necessarily an exceptional one.

The most likely outcome, in my view, produces approximately 13–15% annualized returns over the next decade. The probability-weighted expected return across all five scenarios lands closer to 13–14%. That is a genuinely attractive expected return for a business of this quality. At the same time, it likely falls just short of the type of deeply asymmetric opportunity that defines a truly exceptional entry point for our concentrated portfolio.

In other words, the business quality is arguably better than the valuation opportunity. Visa appears to be priced around fair value - which, for a compounder this durable, is still a far better setup than most businesses ever offer. But fair value is not the same thing as a wide margin of safety, and understanding that distinction matters.

To understand why, we have to look beyond the surface-level narrative and examine what Visa actually is, how it earns its economics, what could impair those economics, and what the next decade could plausibly look like across a range of outcomes. That is the purpose of this memo.

II. What Visa Actually Is

Visa is most commonly described as a payments company, a credit card network, or a financial technology firm. All of these descriptions are technically accurate and analytically insufficient. They describe what Visa does at the surface level - processes card transactions - without capturing what Visa is at the structural level. Visa is a trust and transaction orchestration network that has spent fifty years becoming so deeply embedded in global commerce that the world’s financial system now depends on it to function. That is a different kind of asset than a payments company, and it deserves a different kind of analysis.

Visa does not issue credit cards. It does not extend loans. It does not bear credit risk when consumers fail to pay their bills. What Visa does is operate VisaNet, a real-time transaction processing infrastructure that connects approximately 5 billion payment credentials - the cards, digital wallets, and payment tokens held by consumers - to approximately 175 million merchant locations across more than 200 countries and territories. Every time a consumer uses a Visa-branded payment method, VisaNet authorizes the transaction, clears the payment, and coordinates settlement between the consumer’s bank, the merchant’s bank, and every party in between. This happens in roughly 100 milliseconds, at a rate of approximately 65,000 transactions per second during peak periods, with 99.999% uptime, in every major currency, across every major regulatory jurisdiction on earth. The infrastructure required to do this reliably - the data centers, the fraud models, the regulatory relationships, the legal frameworks, the settlement mechanics, the chargeback systems - took fifty years and hundreds of billions of dollars of collective investment by Visa and its banking partners to build. It cannot be replicated by a startup, a stablecoin issuer, or a technology company working on a five-year horizon.

Visa earns revenue through four streams:

Service revenue is assessed on the nominal dollar volume of payments made using Visa credentials in the prior quarter - roughly 13% of net revenue.

Data processing revenue is earned on each individual transaction processed through VisaNet, regardless of transaction size - roughly 25% of net revenue.

International transaction revenue is earned on cross-border payments, where a consumer in one country pays a merchant in another - roughly 16% of net revenue and historically the highest-margin segment.

And value-added services revenue - the fastest-growing segment and the one that increasingly defines Visa’s investment thesis - is earned through fraud prevention tools, tokenization infrastructure, issuer processing, analytics, consulting, and a growing suite of software services layered on top of the core network.

Client incentives, which are payments Visa makes to banks and large merchants to maintain exclusive or preferred card relationships, reduce gross revenue to produce net revenue. In the first half of fiscal year 2026, Visa generated $22.1 billion in net revenue, grew that figure 16% year over year, and produced non-GAAP net income of approximately $12.5 billion - a non-GAAP net margin of roughly 56%. These are not the economics of a payment processor. They are the economics of a monopoly toll road with a software layer being built on top of it.

The business model’s most important feature is one that rarely receives adequate emphasis: Visa bears no credit risk. When a consumer defaults on their credit card bill, that loss is borne by the issuing bank, not by Visa. Visa has already collected its transaction fee regardless of whether the underlying consumer pays. This structural separation from credit risk means that Visa’s economics do not deteriorate during recessions in the way that bank economics do. Transaction volume may slow modestly during economic downturns, but Visa does not suffer loan losses, write-downs, or balance sheet impairment. During the 2008 financial crisis, while major banks were insolvent or near-insolvent, Visa’s business model proved largely resilient. This characteristic - high revenue growth, elite margins, no credit risk, and recession resistance - is what justifies the premium multiple the market has consistently assigned to Visa throughout its history as a public company.

III. The Moat

A business moat is only useful if you can clearly explain what it is, why it exists, and what could realistically weaken it over time. Too often, investors simply label a company as having a “strong moat” without ever identifying the actual economic mechanisms driving that advantage.

In Visa’s case, the moat is real, but it is not monolithic. It consists of three distinct components, each with a different level of durability and each exposed to different competitive threats. Understanding those distinctions matters, because not all parts of Visa’s competitive position are equally protected, and not all risks deserve the same level of concern.

The first component is network effects. Visa’s network becomes more valuable with every participant added on either side. Consumers carry Visa credentials because they are accepted everywhere. Merchants accept Visa because their customers carry it. Banks issue Visa cards because their customers can use them anywhere. Every new credential issued, every new merchant that accepts Visa, and every new country that integrates into VisaNet makes the network more valuable to every existing participant. This is a self-reinforcing dynamic that has been compounding for fifty years, and the scale it has reached - 5 billion credentials, 175 million merchant locations, 14,500 financial institution clients - makes it extraordinarily difficult for a competitor to challenge meaningfully. A new payment network would need to simultaneously convince enough consumers to carry its credential and enough merchants to accept it to be useful to anyone. This chicken-and-egg problem has defeated numerous well-funded attempts to compete with Visa directly, and it remains the foundation of the moat.

The second component is switching costs embedded in financial institution relationships. Banks, credit unions, and financial technology companies that issue Visa credentials have deeply integrated Visa’s processing infrastructure into their core systems. The certifications, compliance frameworks, chargeback procedures, fraud reporting mechanisms, and settlement protocols that govern a bank’s relationship with Visa are not superficial integrations that can be switched in a quarter. They represent years of technical work, regulatory approval processes, and operational dependencies. The average issuing bank’s core payment processing infrastructure is rebuilt on a decade-plus cycle if it is rebuilt at all, and Visa sits at the center of that infrastructure. This creates a switching cost that is not primarily financial - it is operational and regulatory. The cost of switching is not just a fee. It is the disruption of a mission-critical system during a process that regulators scrutinize carefully.

The third component - and the one that is evolving most rapidly and matters most for the forward-looking investment thesis - is Visa’s global adversarial fraud intelligence graph. Visa processes over 300 billion transactions annually across 200 countries, generating a real-time dataset of transaction patterns, fraud vectors, merchant behavior, consumer behavior, and coordinated attack signatures that no other entity on earth possesses. This dataset is not simply large. It is adversarially diverse in ways that make it qualitatively different from any dataset a single merchant, bank, or regional payment network could assemble. A sophisticated synthetic identity fraud ring operating across forty countries and twelve currencies looks completely different to Amazon’s fraud system - which sees only Amazon transactions - than it does to Visa, which sees the coordinated pattern across the entire global ecosystem. This global visibility is what makes Visa’s fraud intelligence products genuinely non-replicable, and it is the reason that Visa’s Risk and Security segment represents the most durable and most strategically important part of the business. Counterintuitively, AI may strengthen this moat rather than erode it. As AI-driven fraud attacks scale globally, isolated fraud systems with narrower transaction visibility will struggle to defend against coordinated adversarial attacks that span multiple ecosystems simultaneously. The entity with the broadest adversarial visibility becomes more valuable, not less, as the sophistication and scale of fraud attacks increases.

IV. Value-Added Services

Until approximately five years ago, Visa’s investment thesis was simple: global cash displacement would continue, card payment volumes would compound at high single digits annually, Visa would take its toll, and the buyback machine would translate revenue growth into double-digit EPS growth. That thesis remains partially intact. But the more important development of the past five years is the emergence of value-added services as a distinct and increasingly central revenue stream, one that is growing at twice the rate of the core business and whose long-term trajectory will determine whether Visa deserves a premium multiple a decade from now.

Value-added services generated approximately $10.9 billion in fiscal year 2025, up 23% in constant dollars, and now represents approximately 30% of Visa’s net revenue. Since fiscal year 2021, VAS has compounded at roughly 20% annually in constant dollars - more than double the growth rate of core payment revenue. These are not trivial numbers. VAS is already one of the largest and fastest-growing software and services businesses in the world, measured by absolute revenue. The market has not yet fully processed what it means for Visa’s earnings quality, duration, and deserved multiple that 30% of revenue is growing at 20% in software-like products rather than in transaction fees.

VAS consists of four segments with meaningfully different moat profiles:

Issuing Solutions - the largest - includes Visa DPS debit processing, the Pismo cloud-native core banking platform acquired in early 2024 for $929 million, credential management, and tokenization infrastructure. This segment benefits from deep switching costs within banking relationships and compounds reliably at mid-teens rates.

Acceptance Solutions includes the Cybersource enterprise payment gateway, the Authorize.net small business payment platform, and Visa’s Tap to Phone and Unified Checkout products. This segment faces the most competitive pressure from Stripe and Adyen and should be underwritten more conservatively.

Advisory and Other Services includes Visa Consulting and Analytics, marketing services, and increasingly sophisticated advisory work around stablecoins and AI payments - this segment has grown rapidly but contains episodic elements, including notable demand in fiscal year 2026 driven by the FIFA World Cup and Olympic Games. The comparables in fiscal year 2027 will be tougher, and investors should not mistake event-driven consulting revenue for structural acceleration.

The most important segment is Risk and Security Solutions, which includes Visa Advanced Authorization, Visa Risk Manager, Visa Protect for A2A, and the Featurespace AI fraud platform acquired in late 2024 for $946 million. This segment is the center of gravity of the entire VAS story. It possesses the strongest moat, the highest growth potential, the greatest strategic optionality, and the most defensible competitive position against both technological commoditization and large-merchant internalization. Visa Protect for A2A is the product that most directly expresses this segment’s strategic significance: it sells Visa’s fraud intelligence to real-time payment networks and bank-operated payment systems that compete with Visa’s own card rails. In a live production deployment in Brazil, Visa scored approximately $500 billion of Pix transaction volume over six months and identified over $90 million of fraud that could have been prevented, with a detection rate exceeding 80%. That is not a proof of concept. That is a commercial product generating real revenue on a competing rail. It demonstrates precisely the strategic posture that makes the bull case intellectually serious: Visa is not trying to stop competing rails from existing. It is selling them the trust infrastructure they need to scale.

The single most important monitoring metric for the VAS thesis is the relationship between remaining performance obligations and VAS revenue growth. Remaining performance obligations represent Visa’s contracted future revenue: deferred revenue already received plus contract revenue that will be invoiced in future periods. If RPO grows consistently faster than VAS revenue, the contractual backlog is deepening, meaning customers are committing to Visa’s services on multi-year terms rather than purchasing them annually. That is the signature of infrastructure software economics. If RPO growth merely tracks or lags VAS revenue growth, the business mix is shifting toward project-based and episodic revenue - lower quality and deserving of a lower multiple. As of the most recent filing, remaining performance obligations stood at $5.5 billion. Tracking RPO growth relative to VAS revenue growth on a quarterly basis is the most important single indicator of whether the VAS infrastructure thesis is materializing or stalling.

V. The Threats

Four competitive and regulatory forces receive the most attention in discussions of Visa’s long-term prospects, and each deserves an honest rather than dismissive assessment.

Account-to-account payment rails and real-time payment systems - FedNow in the United States, RTP, UPI in India, Pix in Brazil, and equivalent systems proliferating globally - represent the most structurally significant competitive development of the past decade. These systems allow money to move directly between bank accounts without touching a card network, potentially bypassing Visa’s economics entirely. The threat is real but unevenly distributed. Real-time rails most naturally attack domestic debit, recurring low-ticket payments, P2P transfers, and merchant-funded closed-loop payment flows. They are least threatening to cross-border payments, credit transactions, fraud-intensive commerce, high-ticket purchases, and any transaction where dispute resolution, chargeback protection, and consumer liability guarantees matter to the paying party. Visa’s domestic U.S. debit economics will face meaningful pressure over the coming decade. That is a real drag on the business. It is not an existential threat. And as Visa Protect for A2A demonstrates, Visa has already identified the strategic response: sell risk and fraud intelligence to A2A rails rather than compete with them, capturing value from the rail’s growth rather than fighting it.

Stablecoin payment systems represent the more speculative but potentially more significant long-term consideration. Stablecoins - digital currencies pegged to fiat currencies and settled on blockchain infrastructure - could in theory enable direct value transfer between parties without routing through any traditional payment network. Over 130 stablecoin-linked card issuing programs now operate across more than 40 countries using Visa’s infrastructure, and monthly stablecoin Visa card spend has surpassed $2.5 billion. The near-term trajectory is more likely one of coexistence than displacement. The longer-term question - whether stablecoins eventually enable sufficiently trusted direct settlement that bypasses card networks in high-value use cases - remains genuinely unresolved. The probability of severe disintermediation through stablecoins within a decade is low. The probability of meaningful economic pressure on select high-margin cross-border flows is non-trivial and belongs in the bear and left-tail scenario weights.

Agentic commerce - the emerging category in which AI agents transact autonomously on behalf of humans - is simultaneously Visa’s most speculative near-term risk and its most compelling long-term opportunity. If AI agents can transact wallet-to-wallet using stablecoins with identity, fraud protection, and compliance handled entirely outside the Visa network, Visa’s role in those transactions shrinks. But this requires the trust, authentication, and dispute infrastructure currently provided by Visa to be successfully replicated at scale by other parties - a task whose technical and regulatory complexity is routinely underestimated. The more likely scenario is that agentic commerce creates massive new transaction volume that routes through Visa’s infrastructure. Visa has already issued agentic tokens - programmable payment credentials that allow AI agents to transact within defined parameters while maintaining consumer protection frameworks. The strategic direction is correct. The commercial scale is early but observable and growing.

Litigation and regulatory risk deserves a measured rather than alarmed assessment. The interchange multidistrict litigation generated $894 million in new accruals in the first six months of fiscal year 2026 alone. Normalized litigation and regulatory friction should be treated as a permanent cost of approximately $500 million to $1 billion annually pre-tax rather than as a declining drag. The more significant long-term regulatory risk is not a single large settlement but gradual pricing regulation - interchange caps, routing mandates, and competitive access requirements that compress Visa’s pricing power incrementally over time. This belongs in the bear scenario weight as a persistent margin headwind rather than in the left-tail as an existential threat.

VI. The Five Scenarios

Rather than producing a single point estimate of future value - which creates false precision and discourages the kind of probabilistic thinking that sound investment decisions require - this analysis is organized around five distinct scenarios that span the realistic range of outcomes for Visa over the next decade. Each scenario differs not merely in growth rate assumptions but in the fundamental economic role that Visa occupies in global commerce at the end of the decade. The progression from left-tail to super-bull is a progression from Visa losing its premium economics while remaining operationally important, to Visa becoming the universal orchestration layer of all digital value transfer.

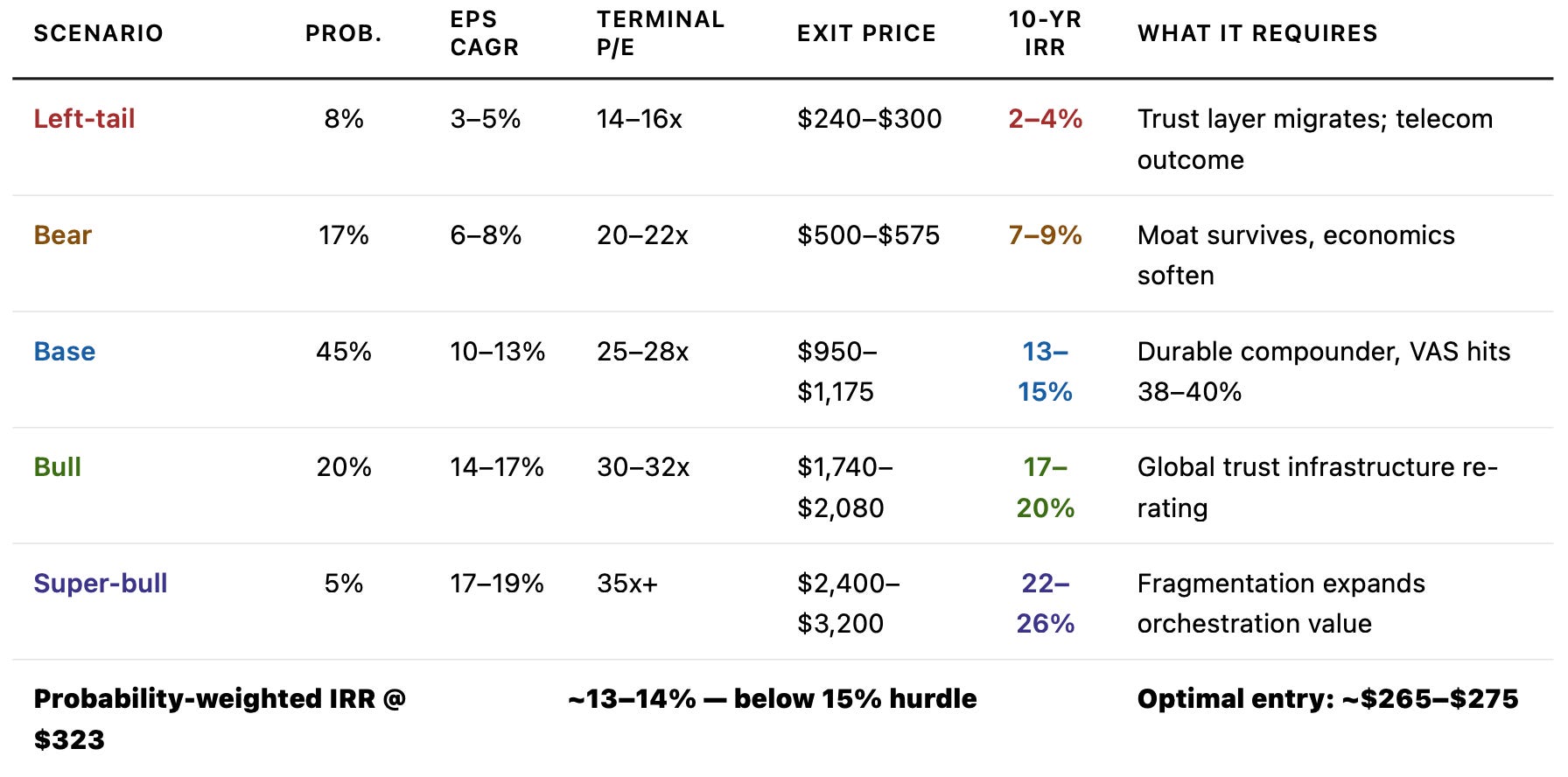

Left-Tail: 8%

Visa remains important but loses premium economics. The telecom outcome. Volume grows. Transaction counts increase. The network processes more payments than ever. But the economics per unit erode steadily as large merchants internalize fraud and identity infrastructure, real-time rails capture domestic debit economics, and the trust layer partially migrates away from Visa. The business becomes utility-priced rather than software-priced. EPS compounds at 3–5% annually. Terminal P/E compresses to 14–16x. 10-year IRR from $323: 2–4%. Exit price: $240–$300. At 2–4% nominal, the left-tail produces negative to flat real returns after inflation - the precise definition of a capital impairment outcome for a long-duration investor, and the scenario the margin of safety framework is specifically designed to prevent. The danger of this scenario is its invisibility - the business looks operationally fine for years before the multiple reprices, trapping investors who correctly identify quality but misread the pace of economic erosion beneath the surface.

Bear: 17%

Visa remains wonderful but compounds slightly slower than required. The moat survives. Management executes competently. VAS grows at 12–15%, not 20–25%. A2A rails pressure domestic debit. Regulatory friction becomes a permanent margin tax. VAS matures into a high-quality services business but never achieves the contracted recurring infrastructure economics that would justify software-like duration assumptions. EPS compounds at 6–8%. Terminal P/E compresses to 20–22x. 10-year IRR from $323: 7–9%. Exit price: $500–$575. The possible danger is psychological - the investor never receives a clean exit signal because the business never actually disappoints by any normal measure. The thesis remains qualitatively intact while the returns quietly disappoint for a decade.

Base: 45%

Visa executes almost perfectly, and the market already prices it that way. Risk and Security sustains 18–22% constant-dollar growth. VAS crosses 38–40% of net revenue organically. Cross-border holds at 12–15% growth. Operating margins remain stable at 65–67%. RPO grows measurably faster than VAS revenue, signaling deepening contractual embeddedness. EPS compounds at 10–13%. Terminal P/E: 25–28x. 10-year IRR from $323: 13–15%. Exit price: $950–$1,175. The base case already assumes something close to excellent execution - it is not the minimum expectation but what happens when management delivers on nearly every dimension of a demanding strategic agenda simultaneously. The investor earns a return that is genuinely good in absolute terms while falling modestly below our 15% hurdle that defines a truly exceptional entry point.

Bull: 20%

Visa successfully transitions into global trust infrastructure. The market spends the first half of the decade fearing what AI, stablecoins, and real-time rails will do to Visa, and spends the second half recognizing that those technologies made Visa more essential rather than less. Risk and Security reaches $15–20 billion in annual revenue with multi-year contracted infrastructure economics. Visa Direct surpasses 30–40 billion annual transactions. VAS crosses 42–47% of net revenue. EPS compounds at 14–17%. Terminal P/E: 30–32x. 10-year IRR from $323: 17–20%. Exit price: $1,740–$2,080. The re-rating is correction, not euphoria - the market updating a misclassification of what kind of business Visa has become, not projecting speculative multiples onto a deteriorating one.

Super-Bull: 5%

Fragmentation itself dramatically expands the value of orchestration. Visa wins because payments fragment. The more payment rails proliferate - cards, stablecoins, RTP systems, AI agent wallets, tokenized deposits - the more indispensable a neutral, trusted, globally embedded orchestration layer becomes. Agentic tokens become a standard credentialing mechanism for AI commerce. Visa Direct reaches 60–80 billion annual transactions. Risk and Security is repriced as multi-year contracted infrastructure across all digital transaction systems. EPS compounds at 17–19%. Terminal P/E: 35x+. 10-year IRR from $323: 22–26%. Exit price: $2,400–$3,200. The 5% probability reflects not doubt about the logic but discipline about the timeline - the world may take longer to converge on this outcome than a ten-year model horizon can capture.

VII. The Probability-Weighted Return Model

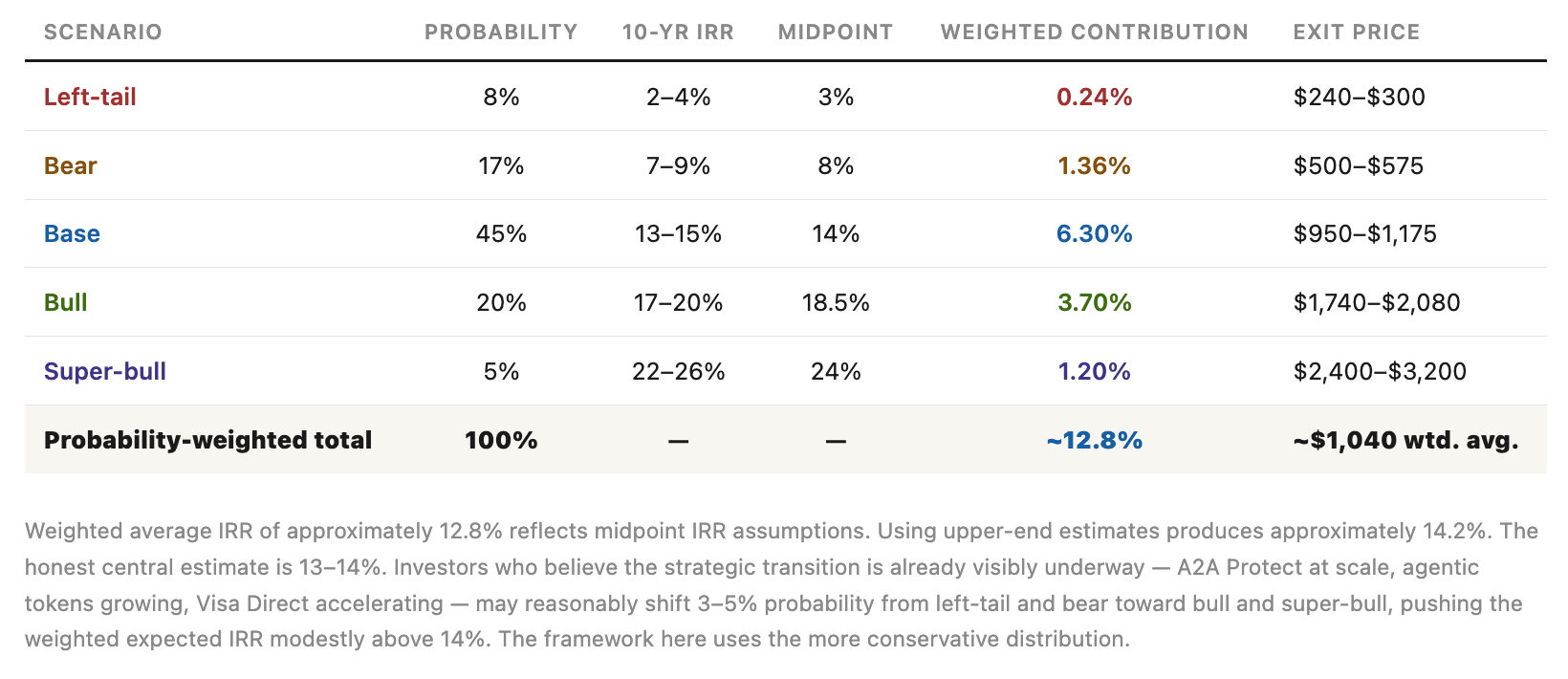

Aggregating the five scenarios into a probability-weighted expected return requires multiplying each scenario's 10-year IRR by its assigned probability and summing the results. This produces a single expected return figure that honestly represents the distribution of outcomes facing an investor who pays $323 today and holds for a decade.

The probability-weighted expected return of approximately 13–14% from $323 is the most honest single answer to the question of what Visa offers at today’s price. It is approximately 800–900 basis points above the current risk-free rate. It reflects a genuinely excellent business with meaningful upside optionality in the bull and super-bull scenarios, meaningful downside risk in the bear and left-tail scenarios, and a base case that produces good but not exceptional returns.

The gap between 13–14% and 15% is not a rounding error. Over a decade, 150 basis points of annual compounding on a meaningful position represents a substantial difference in terminal wealth. The investor who requires 15% to deploy full conviction capital is not being unreasonable. They are acknowledging that the price does not provide the cushion against downside scenarios that a rigorous framework demands. But there is a subtlety worth acknowledging: an investor who believes the bull case probability deserves to be closer to 23–25% - because the strategic transition is already observable in current products, current revenue trends, and current management behavior - will calculate a probability-weighted IRR of approximately 14.5–15.5% from today’s price. That is the range in which reasonable, well-informed investors who have done this work will land, and the difference between 13.5% and 15% is ultimately a question of how much credit you give the visible evidence that Visa’s transition is already underway.

VIII. Entry Price Sensitivity

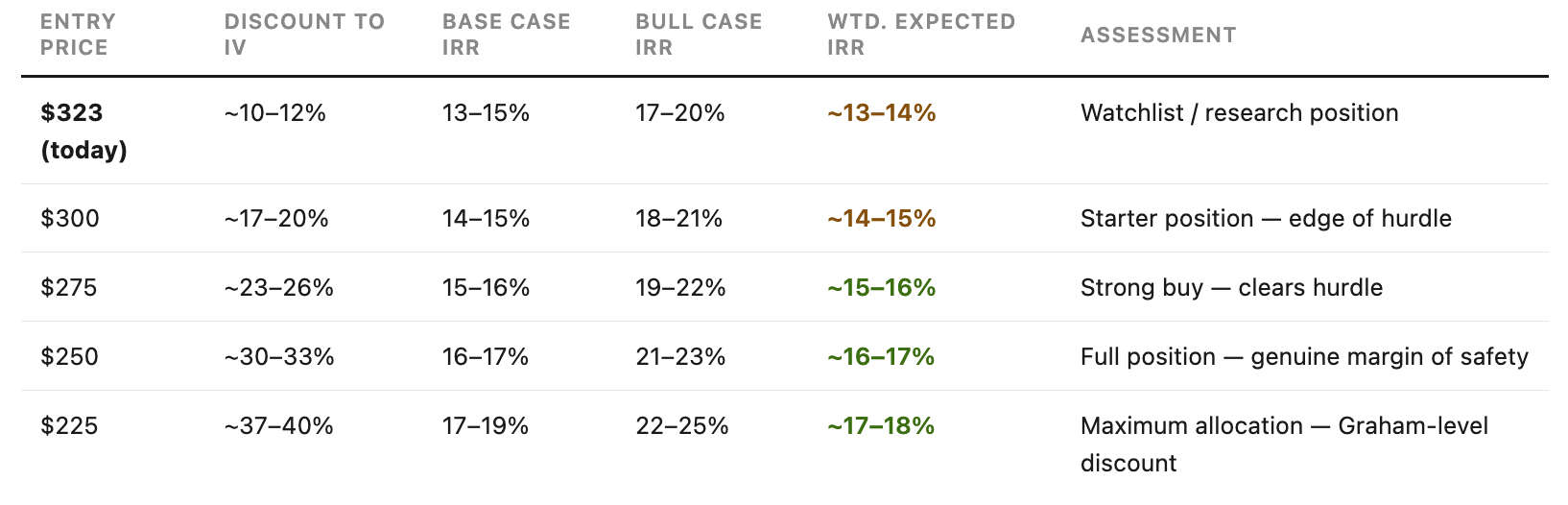

Because the probability-weighted IRR is a function of entry price - lower entry prices improve returns in every scenario simultaneously - the question of what price makes Visa an exceptional investment has a specific mathematical answer.

The table makes clear that the 15% hurdle is cleared at approximately $275 in the base case and at approximately $295–$300 in the probability-weighted expected return framework. At $265–$275, the base case produces 15–16% IRR, the bull case produces 19–22%, and even the bear case produces approximately 10–11% - not ideal but survivable rather than decade-destroying. The margin of safety is not primarily about protecting against business failure. It is about ensuring that even the negative scenarios produce outcomes that preserve capital in real terms rather than destroying a decade of compounding opportunity.

The probability of seeing $265–$275 within the next 24 months requires honest assessment. Visa’s historical peak-to-trough drawdowns include approximately 31% during COVID in early 2020, approximately 23% during the rate spike fears of late 2021 through 2022, and approximately 21% following the DOJ debit antitrust filing in September 2024. A 15–18% drawdown from today’s price - which would bring Visa to the $265–$275 range - is well within the historical volatility range and does not require anything fundamentally wrong with the business. The base case business compounds intrinsic value at roughly 11–12% annually while you wait. The window does not stay open indefinitely on a business compounding this fast. But it is not implausible within a 12–24 month horizon, and the discipline of waiting for it is the operational expression of a margin of safety framework applied to a compounder.

IX. Position Sizing Framework

Position sizing in our concentrated portfolio should emerge from the probability-weighted return distribution and the margin of safety analysis, not from emotional conviction about business quality.

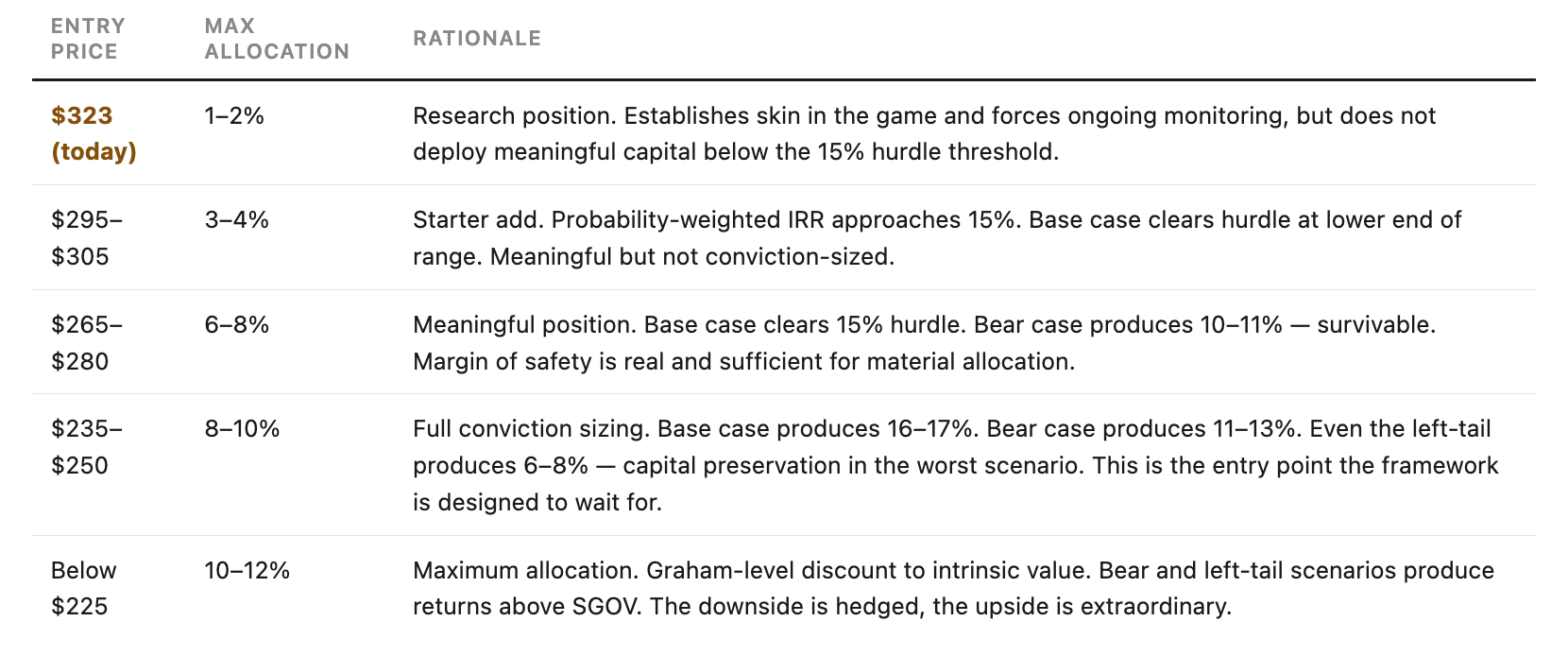

The staged entry framework is not mechanical timidity. It is the quantitative expression of a specific philosophical discipline: that position size should be proportional to the degree of certainty that the investment clears the hurdle, not to the degree of admiration for the business. Visa at $323 is admirable. It is not yet sufficiently discounted to warrant full conviction sizing. Adding to the position as the price declines is not averaging down from weakness - it is deploying capital at the entry points the framework identified in advance as attractive, executing a predetermined plan rather than reacting emotionally to price movements.

X. The Monitoring Dashboard

A long-duration investment is not just about getting the initial underwriting right. Over time, the more important work is watching the business closely enough to determine whether the original thesis is actually playing out as expected. The following metrics are the primary indicators I’ll be watching to assess which scenario appears to be unfolding.

Quarterly - highest priority

Risk and Security constant-dollar growth rate. Base case requires 18%+. Below 15% for two consecutive quarters is an early warning signal. Below 10% for four consecutive quarters is a thesis-break signal requiring full position reassessment.

RPO growth versus VAS revenue growth. RPO consistently outpacing VAS revenue confirms infrastructure economics deepening. RPO tracking or lagging VAS revenue signals a shift toward episodic, project-based business mix.

Net revenue per processed transaction. Stable or growing confirms pricing power intact. Declining for two or more consecutive quarters confirms economic erosion beginning at the transaction layer.

Management language. “Accelerating” and “expanding” describe a business investing in whitespace. “Durable” and “resilient” describe a business defending existing ground. The shift from the former to the latter is a leading indicator of multiple compression, often arriving before the numbers confirm it.

Annual - structural indicators

Cross-border constant-dollar volume growth. Base case requires 12%+. Below 10% for a full fiscal year with management attribution to structural rather than cyclical factors is a bear case signal.

Non-GAAP operating margin trend. Stable at 65–67% confirms the compounding engine is intact. Below 63% for two consecutive years confirms structural margin pressure rather than investment-cycle noise.

Visa Direct transaction growth and progression toward separate revenue disclosure. Sustained above 20% annually confirms new flow monetization expanding. Separate revenue disclosure signals it has crossed from growth metric to core revenue stream - a bull case confirming signal.

VAS mix as percentage of net revenue, assessed in context of total revenue growth. Higher VAS share is unambiguously positive only when total revenue growth remains strong alongside it. VAS mix rising because core payment economics are softening is a quality-degradation signal, not a progress signal.

The most important combined signal:

If Risk and Security growth decelerates below 15% constant dollar for two consecutive quarters while RPO growth simultaneously converges toward or falls below VAS revenue growth, the base case is sliding toward the bear case and the position should be formally reassessed. These two metrics together - the growth rate of the most defensible VAS segment and the contractual depth of the VAS backlog - are the clearest simultaneous indicators of whether Visa's premium multiple is being earned or merely inherited from historical quality.

XI. The Final Conclusion

Visa is, by almost any objective measure, one of the finest businesses ever constructed. The network processes over 300 billion transactions annually across more than 200 countries. The non-GAAP net margin exceeds 55%. The business bears no credit risk. The management team has consistently made rational capital allocation decisions, returning approximately $14 billion to shareholders in the first six months of fiscal year 2026 alone through buybacks and dividends while simultaneously investing in the VAS infrastructure that represents the business’s next chapter. The fraud graph underlying Risk and Security is genuinely non-replicable. The network effects that connect 5 billion credentials to 175 million merchant locations have been compounding for fifty years. The probability of losing money in nominal terms over a decade from today’s price is extremely low. This is not a risky investment in the conventional sense.

And yet. At $323 per share and approximately $617 billion in market capitalization, the investor paying today’s price is not discovering an exceptional business at a discount. They are paying approximately fair value for a business the market has understood and correctly priced for years. The market knows about the network effects. It knows about the margins. It knows about the buybacks. It knows about the VAS opportunity. It knows about the trust layer thesis. The multiple of 28–29 times forward non-GAAP earnings already reflects the expectation of continued excellent execution, sustained premium margins, and a successful VAS transition. The investor today is not getting a discount to those expectations. They are paying for them. Not that Visa is overvalued. Not that the thesis is wrong. But the market has already done the work of discovering this exceptional business, and the price reflects that discovery. The investor arriving today is underwriting the continuation of excellence at massive scale, and that is a different and harder task than discovering excellence in the first place.

The base case - the most likely single outcome, assigned 45% probability - is the scenario where Visa does essentially everything right over the next decade. The base case already assumes something close to excellent execution - it is not the minimum expectation but what happens when management delivers on nearly every dimension of a demanding strategic agenda simultaneously. And the investor who bought at $323 earns approximately 13–15% annually, which is excellent in absolute terms and modestly below the 15% hurdle that defines an optimal entry point for our concentrated portfolio. The investor who treats this as the floor of their expected outcomes has implicitly assumed that the bear case - at 17% probability - is effectively off the table. It is not.

The right conclusion from this analysis is not that Visa should be avoided. It is that Visa should be owned at the right price, sized appropriately to the probability distribution rather than to emotional conviction about quality, and monitored rigorously against the specific metrics that distinguish the base case from the bear case in real time. The right price - the entry point at which the 15% hurdle is cleared in the base case with genuine margin of safety against the bear and left-tail scenarios - is approximately $265–$275. At that entry, the base case produces 15–16% IRR, the bull case produces 19–22%, and even the bear case produces 10–11%. The downside is hedged. The upside is extraordinary. The discipline of waiting for that price is not pessimism about Visa’s quality. It is respect for the mathematics of what margin of safety actually means in our concentrated portfolio where every position must carry its weight.

The final sentence of this analysis is the one that should accompany every investment decision about any exceptional business at any price: an exceptional business is not automatically an exceptional investment. Visa at $265 is both. Visa at $323 is only the first. The distance between those two descriptions, measured in dollars per share, is approximately sixty dollars. The distance between them, measured in decade-long IRR, is the difference between a great investment and a good one. For a concentrated value investor with a 15%+ hurdle and a margin of safety discipline, that is not a small distinction. It is the entire point of the exercise.

Framework Summary:

Disclosure: This memo represents independent investment research and reflects the author's analytical framework and probabilistic assumptions. It is not investment advice. All projections are estimates based on publicly available information including Visa's Form 10-Q for the quarter ended March 31, 2026, earnings call transcripts, Investor Day presentations, and third-party research. Actual results will differ from modeled scenarios. All investors should conduct their own due diligence before making investment decisions.