Don't Sell.

Why Wall Street Gets It Wrong

Walk onto Wall Street and you’ll see flashing tickers, CNBC anchors breathless with “breaking news,” and analysts feverishly updating models because next quarter’s EPS estimate shifted by three cents. It is a temple to the voting machine, not the weighing machine.

The dysfunction is not hard to spot:

Average holding period: In the 1950s, the average NYSE investor held a stock for roughly 8 years. Today, the average holding period is closer to 5–6 months. For many mutual funds and ETFs, turnover is even higher - some measure their holding periods in weeks or days.

Incentives: Managers are rewarded for beating a benchmark in the short term. Underperform for one year, no matter how sensible your strategy, and you risk losing assets or your job.

Performance: Over long spans, the data is damning. According to S&P’s SPIVA studies, roughly 85–90% of actively managed U.S. large-cap equity funds underperform the S&P 500 over 10-year periods, and that figure rises to 88–92% over 15–20 years.

Benchmarks, career risk, constant churn: Because their bonuses, reputations, and businesses depend on showing results quickly, there is enormous pressure to be active - even when patience and passivity would compound wealth far better.

And yet, there is already a proven road map to success.

Buffett’s Partnership (1957-69) delivered ~25% annual returns vs ~8% for the broader market. Nomad compounded at ≈20%+ per year by doing almost nothing. Pulak Prasad’s Nalanda similarly follows a path of robustness: no leverage, avoid turnarounds, stay in stable industries, “let compounding do the work”.

So why does almost no one follow this path?

Because it’s slow.

Because it’s boring.

Because ambition and incentives push for action, not patience.

The Lesson of the Terminal Portfolio: Never Sell (or Very Rarely)

There is a particular virtue in never selling, or in maintaining a portfolio that is “terminal” - meaning, you buy, hold, let compounding work, and you don’t sell out of panic, market noise, or shifts in fashion.

Two powerful modern examples:

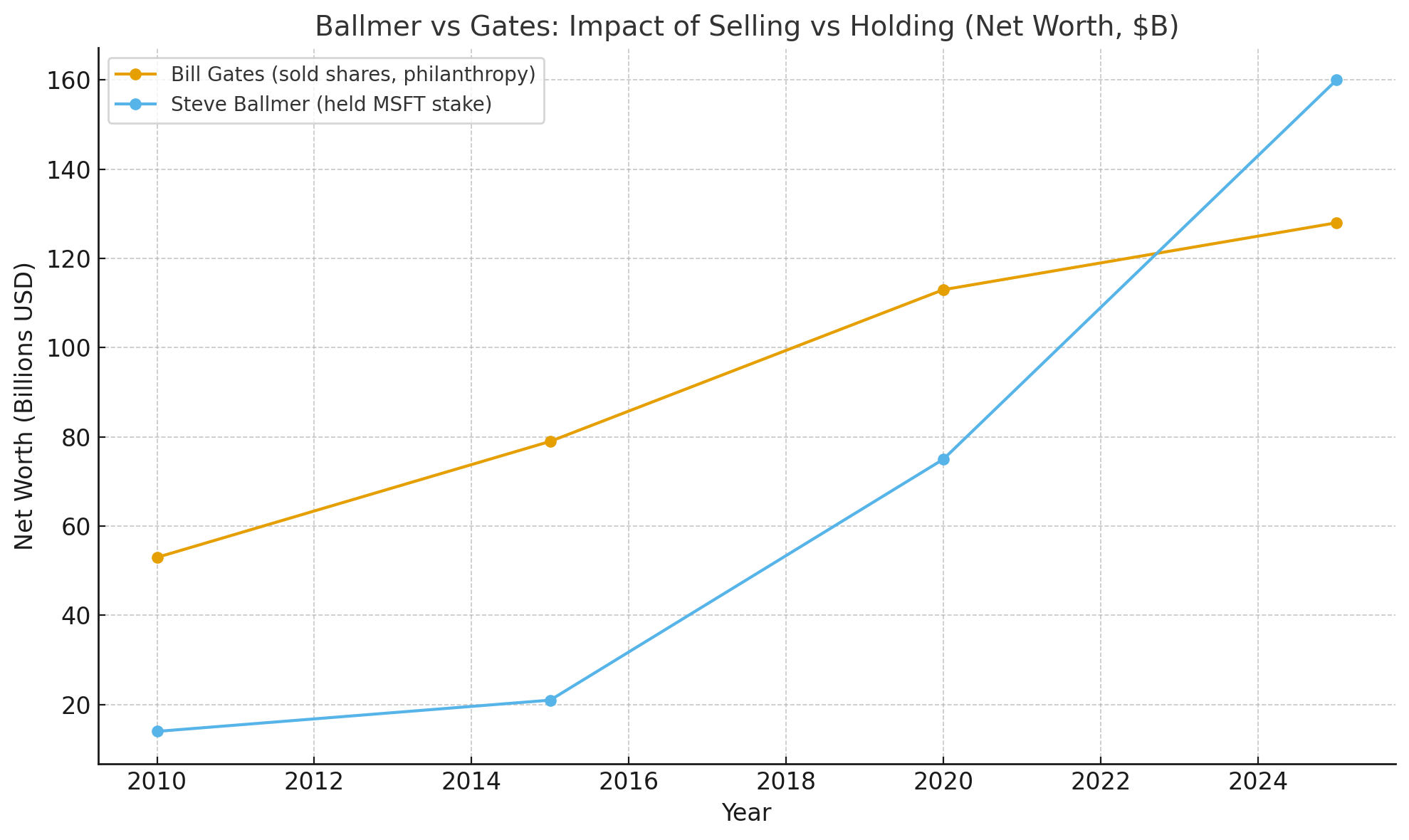

1. Steve Ballmer vs Bill Gates

Steve Ballmer, former CEO of Microsoft, holds a huge stake in Microsoft that he never sold (or very minimally sold). As of mid-2025, Ballmer’s net worth is estimated around US$150-170 billion, with “more than 90% of Ballmer’s wealth in Microsoft shares.”

Bill Gates, though a cofounder, has given away or sold very large portions of his Microsoft shares over the decades (for philanthropy, taxes, diversification, etc). Because of those sales and shifts in his portfolio and focus, his net worth has dropped relative to Ballmer’s, especially when Ballmer’s shares have ridden Microsoft’s growth in cloud, enterprise, and AI.

The contrast illustrates that if you trust in a great business and you avoid selling, you let the wealth build exponentially. Selling (especially early or often) gives up a lot of that upside.

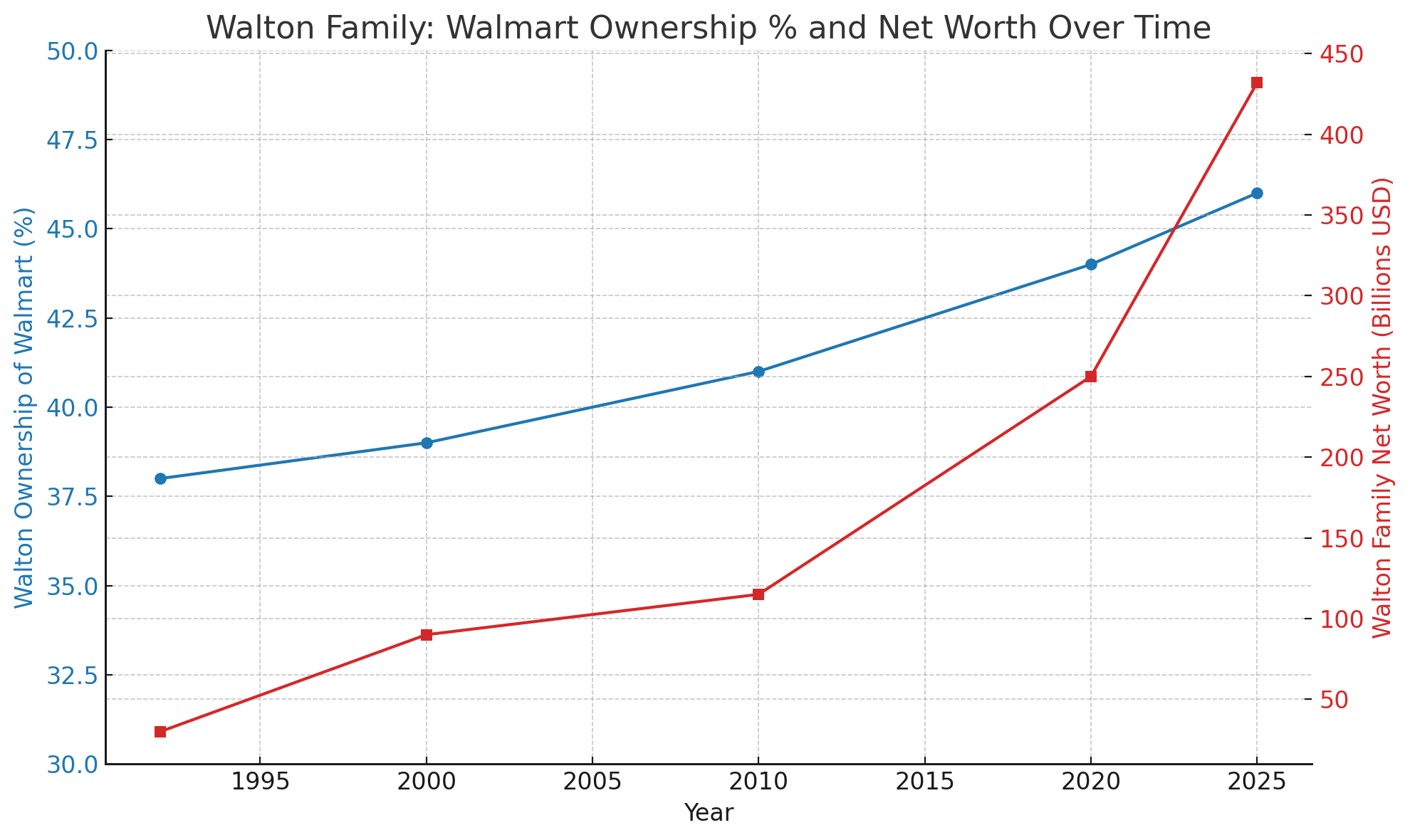

2. Walton Family and Walmart

The Walton family heirs (Jim, Rob, Alice Walton) inherted roughly 38% of Walmart, however, they currently own about 45-46% of Walmart via Walton Enterprises LLC and their trusts.

For decades, Walmart has returned excess cash to shareholders (including the Waltons) via stock buybacks - which reduces the share count, raising each remaining owner’s slice of the pie. Even without increasing the share percentage by acquiring new shares, when a company does buybacks, your effective ownership of the profits and equity grows.

As of 2025, the Walton family’s net worth is estimated at ~US$432 billion, making them the richest family in the U.S. - and globally, by many counts.

What these examples teach:

Having ownership in a business and staying invested long term matters much more than frequent trading.

Buybacks amplify the power of never selling: if a business produces excess earnings, uses them to reduce share count instead of distributing them all, then the value for the long-term owner compounds even better.

Selling dilutes that effect: each sale locks in gains (or losses), and forfeits the upside that might come in subsequent growth years.

Putting It All Together: What You Should Do

If you want to be a great investor, or run a portfolio that matters in compounding over decades, here’s a prescription:

Build a terminal portfolio - hold exceptional businesses, preferably ones with durable competitive advantages, minimal leverage, strong management.

Do not sell, unless fundamental change in business, or you find something clearly better. Avoid selling for portfolio rebalancing (unless gross misalignment).

Let compounding + buybacks + growth do the heavy lifting. These are slow processes, but they win over time.

Ignore the voting machine - daily price moves, short-term consensus, performance metrics. Focus on the weighing machine: intrinsic value, business cash flow, reinvestment.

A Note of Caution

Does this mean you should buy any business and hold it forever? Not at all. Forever is only a good idea if you start with the right business. As Charlie would put it: “If you buy a bad business, time is the enemy. If you buy a good business, time is your friend.”

The lesson here is not “never sell under any circumstances,” but rather: when you do find a truly exceptional business - one with enduring competitive strengths, honest and capable management, and the ability to reinvest at high rates of return - the worst mistake you can make is to let it go too soon.

As for defining a “high-quality business”? That’s a topic worth its own letter.

| A guest post by

|